- Save

- Invest

- Borrow

- Pay

- More

- Customer Services

Secured vs. Unsecured Loans: What's the Difference?

Understanding the key differences between secured vs unsecured loans.

Key Takeaways

- You can avail of two types of loans – Secured and Unsecured loan.

- Banks extend secured loans against collateral or security.

- In the case of Unsecured Loans, banks do not ask for collateral.

- Secured Loans are ideal for lower loan amounts, whereas banks provide unsecured loans for higher loan amounts.

- Interest rates offered on unsecured loans is higher than those on secured loans.

Life is unpredictable, and you might need to rely on financial aid to meet certain unforeseen expenses. To meet such financial challenges, you can rely on bank loans. While there are several kinds of loans that help you fulfil different requirements, in general, banks broadly classify loans into two types – secured and unsecured Loans. Find out what is secured and unsecured loan in this article.

Secured vs Unsecured Loan

Applying for a loan can help you cover financial gaps or achieve major life goals requiring funds on urgent basis. Both secured and unsecured loan have different terms and functionality. Let’s understand these types of loan in depth.

What is a Secured Loan?

A secured loan is a type of loan that requires the borrowers to submit a collateral which can be property, gold, investment certificates, etc. The bank provides the loan amount against this collateral. DBS Bank offers secured loans such as Loan Against Property which offers low processing fees and interest rates as low as upto 10% p.a.

What is an Unsecured Loan?

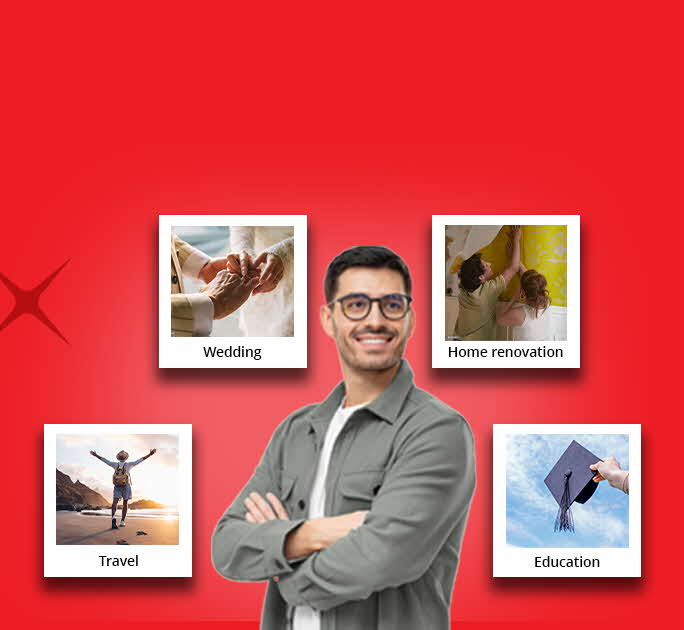

An unsecured loan is generally preferred when the borrower requires an instant personal loan without providing collateral. The banks the borrower’s income, credit history and other factors before sanctioning the loan amount. This type of loan can be used for various purposes such as weddings, home renovations and emergencies. Aside from personal loans, credit cards are also unsecured loans that allow you to use the credit limit set by the bank.

DBS Bank offers personal loans for salaried employees as well as self-employed professionals with low interest rates and flexible EMI terms.

Secured Loan vs Unsecured Loans: Difference

To decide whether secured or unsecured loan would be the best option for you, it’s important to understand the difference between secured loan and unsecured loan. Refer to the below table to understand the function and features offered by both loans.

|

Feature |

Secured Loans |

Unsecured Loans |

|

Borrowing Limits |

Higher loan amounts, due to collateral requirement |

Lower loan amounts as no collateral is required |

|

Rate of Interest |

Lower interest rates due to collateral |

Higher interest rates to offset bank’s risk |

|

Bank’s Risk |

Lower risk for bank; collateral can be auctioned in case of default |

Higher risk as there's no collateral to fall back on |

|

Repayment Tenure |

Longer tenures (e.g., up to 30 years for home loans) |

Shorter tenures (e.g., up to 60 months for Personal Loans, 84 for Auto Loans) |

|

Collateral Requirement |

Collateral is mandatory |

No collateral required |

|

Approval Process |

Takes longer due to collateral verification and documentation |

Faster approval as fewer documents are required |

|

Loan Amount Flexibility |

More flexible with higher amounts based on asset value |

Limited flexibility in loan amount |

|

Processing Time |

Slower due to asset evaluation and paperwork |

Typically, quicker processing |

When applying for loan, it’s important to consider the purpose of the loan and the application process for both secured and unsecured loans. It’s important to check with your bank on the different types of secured and unsecured loan options available. Also factor in the tenures, interest rates and the application process for loans provided by the bank.

For secured loans, it is important to check what type of asset the bank will accept as collateral and what is the maximum loan-to-value ratio offered by the bank.

When it comes to unsecured personal loans, consider using the personal loan eligibility calculator to determine the loan amount you are qualified to borrow.

Secured Vs Unsecured Loan: Which Is Better?

Secured Loans such as home loans come with longer repayment tenures of up to 30 years. Unsecured loans like Personal Loans or Auto Loans come with shorter repayment tenures of 60 months and 84 months, respectively.

Apply for Secured and Unsecured Loans with DBS Bank

With DBS Bank, you can apply for secured and unsecured loans conveniently. You can provide assets as collateral and get higher borrowing limits on unsecured loans. You can just as easily avail of secured loans by providing your credit report featuring good credit scores. So, whether you need a Car Loan, a Loan Against Property, or any other loan, you can visit DBS Bank to begin the loan application process.

Download the digibank by DBS app to get started and even open your savings account with us.

*Disclaimer: This article is for information purposes only. We recommend you get in touch with your income tax advisor or CA for expert advice.

Keep Reading

Read more about our Products & Service

Our Products

- Savings Account

- Personal Loan

- Fixed Deposit

- Recurring Deposit

- Remittance

- Mutual Fund

- SIP

- Debit Card

- Bill Payment

- Internet Banking

- Travel Now

- PRIME Savings Account

- Safe Deposit Locker

Need Help?

- Calling from India:

1860 210 3456 / 1860 267 4567 - Calling from Overseas:

+91 44 6685 4555 - Help & Support

- Grievance Redressal

- Get in Touch with Us

Interest Rates & Calculators

- FD Interest Rates

- RD Interest Rates

- Personal Loan Interest Rates

- Savings Account Interest Rates

- Savings Account Interest Calculator

- FD Calculator

- RD Calculator

- Mutual Fund Calculator

- EMI Calculator

- SIP Calculator

- Lumpsum Calculator

- Financial Goal Calculator

- Monthly Investment Calculator

- ELSS Calculator

- Personal Loan EMI Calculator

Open Instant DBS Bank Savings Account

Useful Links

- About DBS

- Rates & Fees

- In the News

- Forms & Legal

- Grievance Redressal

- Anti-Malware Security Features

- Cyber Security

- Savings Schedule of Benefits

- Schedule of Charges

- KYC FAQs

- DBS Mobile Checksum

- Sitemap

- List of Recovery Agency

- List of Repossessed Properties

- Financial Inclusion

- Digital Lending Partnership CRED

- Co-lending partnership HCIN