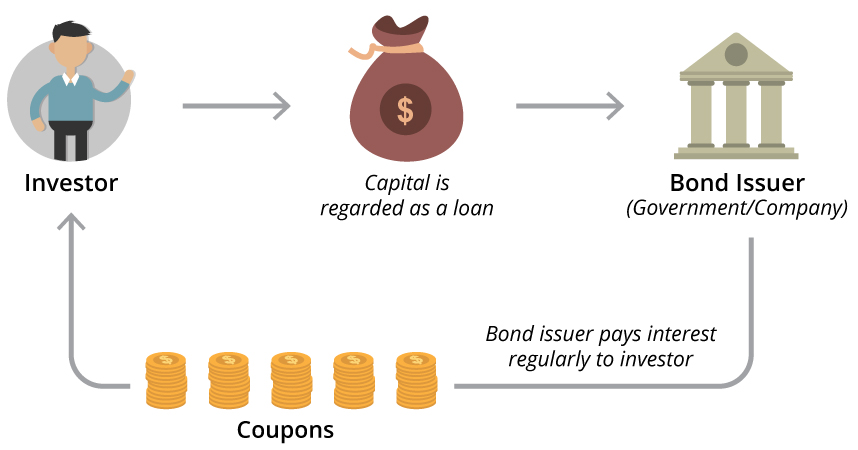

Bonds are debt instruments. When you buy a bond, you are lending money to the company or government institution issuing the bond for a fixed rate of return. It is, in that sense, bonds are legally sophisticated ‘IOUs’, which can be traded between investors.

Typically, in a traditional bond, there is a coupon, which may be regarded as the interest you receive for lending your money. The coupons are paid at fixed intervals, quarterly, semi-annually or annually. As this becomes a source of regular income for the investor, bonds are also known as Fixed Income products.

Generally, the greater the risk, the higher the amount of coupon you should receive to compensate you for lending your capital to a borrower with poorer credit quality. Similarly, bonds with longer lending periods tend to have higher amounts of coupon.

At the maturity date, which marks the end of the term of the bond, there is a legal obligation on the bond issuer to repay the principal amount invested.

Understanding Bond Terminology

|

Par value |

The par value or the face value of a bond is the amount that the bond issuer has borrowed from the investor. |

|

Coupon |

The fixed rate of interest to be paid by the bond issuer to the investor multiplied by the par value of the bond. For example: |

|

Fixed Income |

The amount received in coupons at regular intervals is the investor’s fixed income per year. |

|

Current yield |

Bonds are typically tradeable. As market prices vary from the par value, the current yield of a bond is the annual interest payments of the bond divided by the bond’s current market price. |

|

Callable |

This means the issuer can buy back the bonds earlier than the maturity date, paying investors the principal. |

|

Step-up |

This means the coupon payable rises on a set date. |

Benefits of Bonds

|

|

The fixed income |

|

|

The repayment of the principal |

|

|

The stabilising effect on a portfolio of financial assets |

|

|

Legal obligation on bond issuers |

Risks of Bonds

|

|

Default risk |

|

|

Mark to market risk |

|

|

Interest rate risk |

|

|

Liquidity risk |

DBS Bank offers Mutual Funds that are instant, paperless, signatureless – even transaction fee-less! What’s more? You get to choose from 250+ Mutual Funds across 15 top-performing asset management companies. So why wait? Login to digibank (app or internet banking) and start investing in a flash with instant Mutual Funds on DBS Bank.

Read up more on Mutual Funds here

Mutual Fund investments are subject to market risks, read all scheme related documents carefully before investing.