- Banking

- Wealth

- NRI Banking

- Customer Services

Related Insights

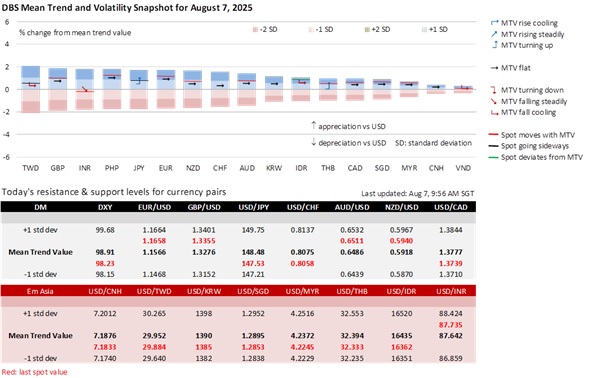

The USD saw losses against all G10 currencies overnight, as markets turn wary of risks to US growth as reciprocal tariffs kick in today. The DXY index has eased towards 98, after softer payrolls and ISM services underscores the negative economic impact from tariffs and associated trade uncertainty. The USD is also likely to be weighed by Fed rate cut expectations, with markets now pricing in a 95% chance of a Fed rate cut in Sep, up from 40% just a week ago.

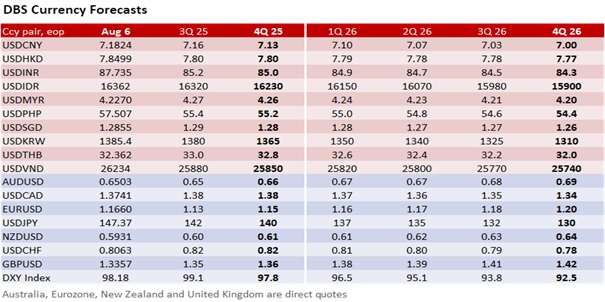

Trump announced that he plans to introduce sectoral tariffs soon with a 100% tariff rate on semiconductors, and a small initial tariff on pharmaceuticals that will eventually be raised to 150%, and finally to 250%. Importantly, countries which had acceded to trade deals with Trump, including Japan and Korea, could enjoy significantly lower tariffs for their semiconductor exports. This implies a remarkable competitive advantage for both compared to other Asian economies. Korea has already highlighted that its semiconductor companies will not face the 100% tariff rate, and we expect both KRW and JPY to be resilient, or even appreciate, despite these sectoral tariffs. On the other hand, RMB may be on the backfoot against regional peers, though China’s trade truce with the US is likely to be extended.

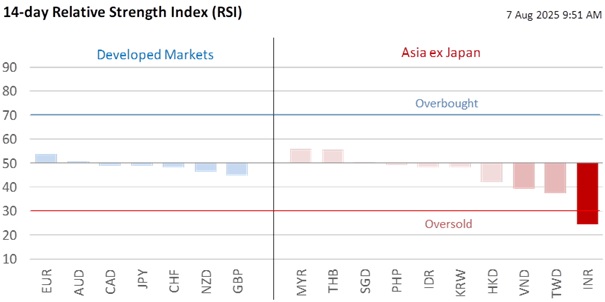

India could see a doubling of its US tariff rate in the coming weeks, with Trump announcing a secondary tariff rate of an extra 25% due to India’s purchases of Russian oil. India may not be the only country purchasing Russian oil, but Trump is certainly looking for ways to pressure Russia, having threatened Russia with further economic sanctions if it does not agree to a ceasefire by this Friday. As such, US secondary tariffs imposed on India may not be easily negotiated away without a broader geopolitical deal, or a complete stoppage of Russian oil imports. Meanwhile, media reports indicate that Indian mobile exports to the US will not face either the reciprocal tariff or secondary tariff but are subject to the forthcoming semiconductor sectoral tariff. USD/INR could hold above mid-87 levels amid elevated secondary tariff risks.

Chang Wei Liang

FX & Credit Strategist

[email protected]Quote of the Day

“If I see three oranges, I have to juggle. And if I see two towers, I have to walk.”

Philippe Petit

August 7 in history

In 1974, French Philippe Petit walked a tightrope strung between the Twin Towers of the World Trade Center in New York City at a height of 1,350 feet.

Topic

GENERAL DISCLOSURE/ DISCLAIMER (For Macroeconomics, Currencies, Interest Rates)

The information herein is published by DBS Bank Ltd and/or DBS Bank (Hong Kong) Limited (each and/or collectively, the “Company”). It is based on information obtained from sources believed to be reliable, but the Company does not make any representation or warranty, express or implied, as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions expressed are subject to change without notice. This research is prepared for general circulation. Any recommendation contained herein does not have regard to the specific investment objectives, financial situation and the particular needs of any specific addressee. The information herein is published for the information of addressees only and is not to be taken in substitution for the exercise of judgement by addressees, who should obtain separate legal or financial advice. The Company, or any of its related companies or any individuals connected with the group accepts no liability for any direct, special, indirect, consequential, incidental damages or any other loss or damages of any kind arising from any use of the information herein (including any error, omission or misstatement herein, negligent or otherwise) or further communication thereof, even if the Company or any other person has been advised of the possibility thereof. The information herein is not to be construed as an offer or a solicitation of an offer to buy or sell any securities, futures, options or other financial instruments or to provide any investment advice or services. The Company and its associates, their directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned herein and may also perform or seek to perform broking, investment banking and other banking or financial services for these companies. The information herein is not directed to, or intended for distribution to or use by, any person or entity that is a citizen or resident of or located in any locality, state, country, or other jurisdiction (including but not limited to citizens or residents of the United States of America) where such distribution, publication, availability or use would be contrary to law or regulation. The information is not an offer to sell or the solicitation of an offer to buy any security in any jurisdiction (including but not limited to the United States of America) where such an offer or solicitation would be contrary to law or regulation.

[#for Distribution in Singapore] This report is distributed in Singapore by DBS Bank Ltd (Company Regn. No. 196800306E) which is Exempt Financial Advisers as defined in the Financial Advisers Act and regulated by the Monetary Authority of Singapore. DBS Bank Ltd may distribute reports produced by its respective foreign entities, affiliates or other foreign research houses pursuant to an arrangement under Regulation 32C of the Financial Advisers Regulations. Where the report is distributed in Singapore to a person who is not an Accredited Investor, Expert Investor or an Institutional Investor, DBS Bank Ltd accepts legal responsibility for the contents of the report to such persons only to the extent required by law. Singapore recipients should contact DBS Bank Ltd at 65-6878-8888 for matters arising from, or in connection with the report.

DBS Bank Ltd., 12 Marina Boulevard, Marina Bay Financial Centre Tower 3, Singapore 018982. Tel: 65-6878-8888. Company Registration No. 196800306E.

DBS Bank Ltd., Hong Kong Branch, a company incorporated in Singapore with limited liability. 18th Floor, The Center, 99 Queen’s Road Central, Central, Hong Kong SAR.

DBS Bank (Hong Kong) Limited, a company incorporated in Hong Kong with limited liability. 11th Floor, The Center, 99 Queen’s Road Central, Central, Hong Kong SAR.

Virtual currencies are highly speculative digital "virtual commodities", and are not currencies. It is not a financial product approved by the Taiwan Financial Supervisory Commission, and the safeguards of the existing investor protection regime does not apply. The prices of virtual currencies may fluctuate greatly, and the investment risk is high. Before engaging in such transactions, the investor should carefully assess the risks, and seek its own independent advice.