- Banking

- Wealth

- Privileges

- NRI Banking

- Treasures Private Client

Related Insights

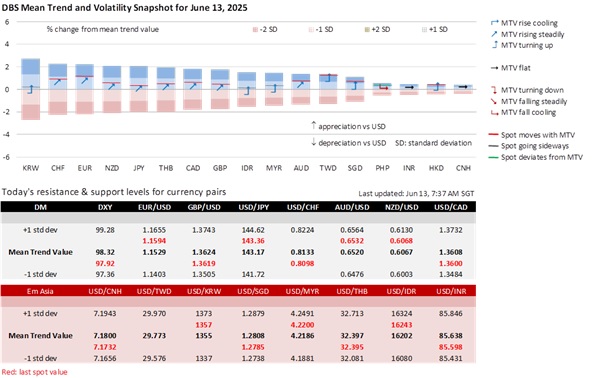

Middle East geopolitical risks are rising after news of an airstrike by Israel on Iran on Thursday, though there are no details of what the targets were. This is in the wake of limited progress in talks between US and Iran on curtailing the latter’s nuclear program. Markets will carefully assess risks of an escalation. Safe havens such as CHF and JPY have rallied, with USD/CHF breaking below 0.81 and USD/JPY easing below 143. Meanwhile, the risk-sensitive AUD has fallen below 0.65, and other risky assets could also see a pare back.

Trump’s plan to announce unilateral tariffs in the next 1-2 weeks has renewed selling pressures on the USD, with the DXY breaking below 98 for the first time since March 2022. His purported ‘Liberation Day’ tariffs have only reinforced the desire of foreign investors to liberate themselves from erratic US trade policy by paring and hedging their USD assets. EUR has been the prime beneficiary of such diversification outflows from the USD, with EUR/USD now surging to 1.16, a level it last saw in 2021.

Export-oriented North Asian currencies are the best performers in Asia on the unilateral tariff news, with KRW, TWD, and JPY gaining between 0.7%-1.0% yesterday. This may seem contradictory given their high dependence on exports, but Korea, Taiwan, and Japan hold a large amount of USD assets due to many years of current account surpluses. North Asian investors are thus actively evaluating the risks to their capital, as the US retreats from international trading norms that have served US capital markets so well in the past. To help insurers with large USD assets manage a falling USD/TWD, Taiwan’s Financial Supervisory Commission will now allow insurers to use 6-month average exchange rates for calculating risk-based capital in their financial reports, instead of the closing exchange rate for the period. Insurers’ liabilities are very long dated, and thus we do not expect insolvency risks to arise from TWD appreciation.

USD/CNH has eased towards 7.17 amid broader USD weakness, helped by improving sentiment after US and China reached an agreement to a trade framework, in principle. Meanwhile, China’s real estate financing stresses may be turning a corner. A real estate developer is looking to tap offshore USD bond markets, which will be the first time a private developer has done so since the start of China’s real estate downturn. PBOC rate cuts and easing HKD liquidity, which are being supported by inflows out of the USD, should buttress sentiment towards China real estate.

Chang Wei Liang

FX & Credit Strategist

[email protected]Quote of the Day

“Strong minds discuss ideas, average minds discuss events, weak minds discuss people.”

Socrates

June 13 in history

In 1373, the Anglo-Portuguese Treaty of Perpetual Alliance (the world's oldest still in existence) was signed in London between King Edward III of England and King Ferdinand I of Portugal.

Topic

GENERAL DISCLOSURE/ DISCLAIMER (For Macroeconomics, Currencies, Interest Rates)

The information herein is published by DBS Bank Ltd and/or DBS Bank (Hong Kong) Limited (each and/or collectively, the “Company”). It is based on information obtained from sources believed to be reliable, but the Company does not make any representation or warranty, express or implied, as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions expressed are subject to change without notice. This research is prepared for general circulation. Any recommendation contained herein does not have regard to the specific investment objectives, financial situation and the particular needs of any specific addressee. The information herein is published for the information of addressees only and is not to be taken in substitution for the exercise of judgement by addressees, who should obtain separate legal or financial advice. The Company, or any of its related companies or any individuals connected with the group accepts no liability for any direct, special, indirect, consequential, incidental damages or any other loss or damages of any kind arising from any use of the information herein (including any error, omission or misstatement herein, negligent or otherwise) or further communication thereof, even if the Company or any other person has been advised of the possibility thereof. The information herein is not to be construed as an offer or a solicitation of an offer to buy or sell any securities, futures, options or other financial instruments or to provide any investment advice or services. The Company and its associates, their directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned herein and may also perform or seek to perform broking, investment banking and other banking or financial services for these companies. The information herein is not directed to, or intended for distribution to or use by, any person or entity that is a citizen or resident of or located in any locality, state, country, or other jurisdiction (including but not limited to citizens or residents of the United States of America) where such distribution, publication, availability or use would be contrary to law or regulation. The information is not an offer to sell or the solicitation of an offer to buy any security in any jurisdiction (including but not limited to the United States of America) where such an offer or solicitation would be contrary to law or regulation.

[#for Distribution in Singapore] This report is distributed in Singapore by DBS Bank Ltd (Company Regn. No. 196800306E) which is Exempt Financial Advisers as defined in the Financial Advisers Act and regulated by the Monetary Authority of Singapore. DBS Bank Ltd may distribute reports produced by its respective foreign entities, affiliates or other foreign research houses pursuant to an arrangement under Regulation 32C of the Financial Advisers Regulations. Where the report is distributed in Singapore to a person who is not an Accredited Investor, Expert Investor or an Institutional Investor, DBS Bank Ltd accepts legal responsibility for the contents of the report to such persons only to the extent required by law. Singapore recipients should contact DBS Bank Ltd at 65-6878-8888 for matters arising from, or in connection with the report.

DBS Bank Ltd., 12 Marina Boulevard, Marina Bay Financial Centre Tower 3, Singapore 018982. Tel: 65-6878-8888. Company Registration No. 196800306E.

DBS Bank Ltd., Hong Kong Branch, a company incorporated in Singapore with limited liability. 18th Floor, The Center, 99 Queen’s Road Central, Central, Hong Kong SAR.

DBS Bank (Hong Kong) Limited, a company incorporated in Hong Kong with limited liability. 11th Floor, The Center, 99 Queen’s Road Central, Central, Hong Kong SAR.

Virtual currencies are highly speculative digital "virtual commodities", and are not currencies. It is not a financial product approved by the Taiwan Financial Supervisory Commission, and the safeguards of the existing investor protection regime does not apply. The prices of virtual currencies may fluctuate greatly, and the investment risk is high. Before engaging in such transactions, the investor should carefully assess the risks, and seek its own independent advice.