- Banking

- Wealth

- NRI Banking

- Customer Services

- Brighter outlook for China equities; re-rating story at early innings, tailwinds at play

- Structural recovery underpinned by capital allocation to onshore equities

- Wealth rebalancing into capital markets to persist

- Prefer tech leaders, beneficiaries of domestic consumption pickup, dividend-yielding financials

Related Insights

- DBS Stock Pulse: (1) Global Technology - Nvidia’s USD5bn bet accelerates Intel’s turnaround (2) Hongkong Land - Punching above SGD7 amid value unlocking progress19 Sep 2025

- DBS Stock Pulse: (1) Market view - 3 implications from the Fed’s measured cut (2) Global Technology Stocks - 7 stocks to watch as China accelerates its self-reliance agenda (3) Equity Picks: Remove Keppel REIT from Dividend18 Sep 2025

- Equities Weekly: European Banks – Beneficiaries of a Steepening Yield Curve17 Sep 2025

Momentum builds. Growth momentum and investment sentiment towards China’s onshore equities have remained robust in 2025, as investors look beyond concerns about the relatively muted near-term economic outlook, the noise suggesting that the liquidity-driven rally may be over, and the views questioning whether a scenario similar to the 2015 sell-down could repeat.

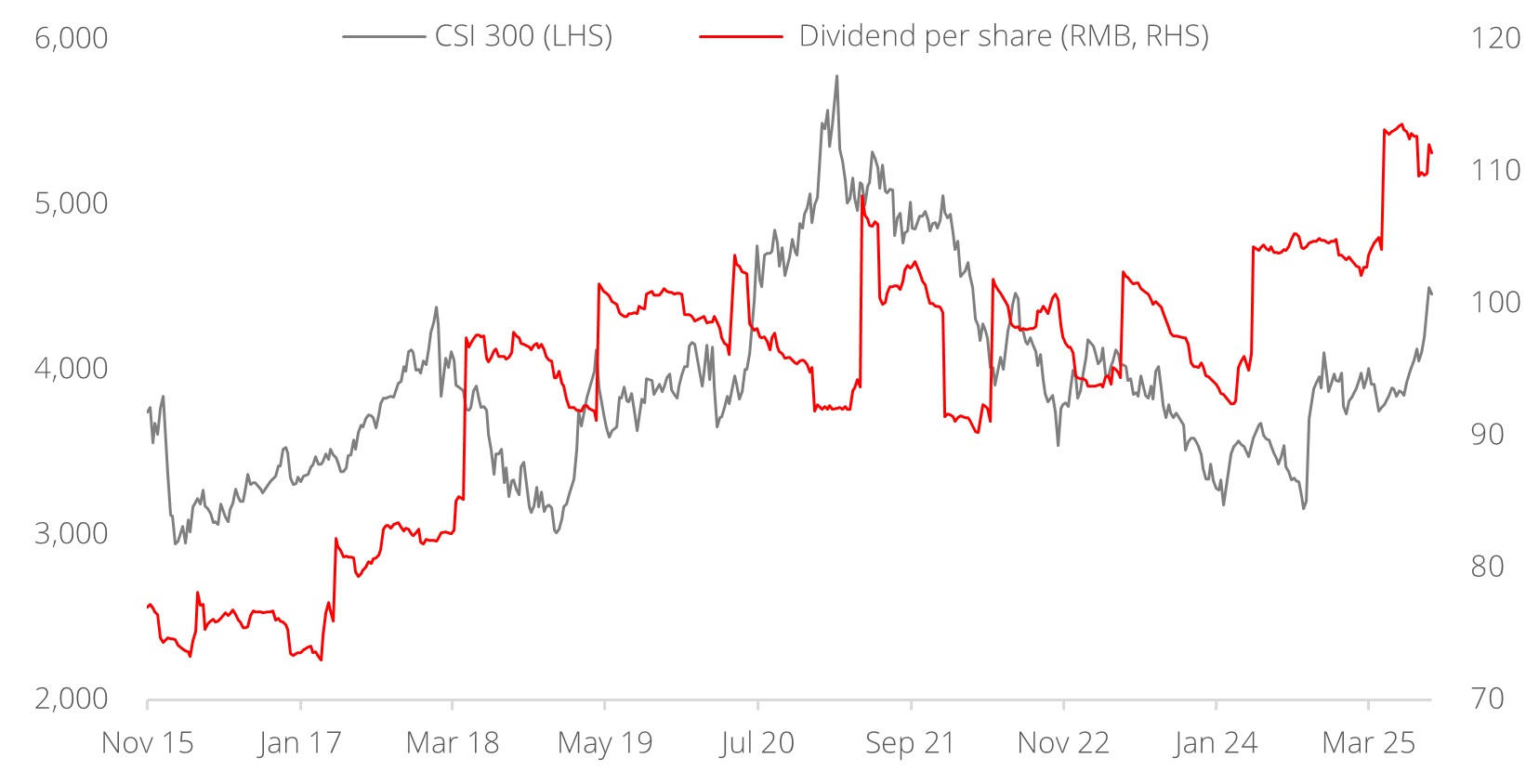

We believe the re-rating story for China equities is at its early innings and buoyed by several tailwinds. Chinese companies are reporting more resilient financials despite lingering near-term economic headwinds, as reflected in the upward trend of dividend per share (Figure 1). Additionally, there is significant potential for the country’s household wealth, currently heavily concentrated in deposits and real estate, to rebalance into capital markets. Against this backdrop, we see an increasingly brighter outlook for China equities, including onshore markets.

We maintain a constructive stance on China equities given structural improvements. Timely and controlled regulatory interventions should progressively reduce unwanted market volatility and enhance the investability of the A-share market. This should in turn facilitate the reallocation of household wealth into the equity market and drive a structural rally. Further progress in China’s economic reforms, efforts under the anti-involution campaign, and a progressively stabilising fundamental outlook among listed companies should also reinforce this trend.

Focus on sectors poised for strong performance. We reiterate our preference for new economy sectors (domestic technology), under-valued cyclicals, and companies set to benefit from a resurgence in consumer spending.

- Technology, particularly platform companies and those involved in the upstream portion of the A.I. value chain (e.g. foundries/chip designers, AI processors, data centers, robotics), are poised to ride on China’s shift towards innovative sectors and benefit from capex-heavy plans by both US and China hyperscalers. The development of cutting-edge foundry capacity underscores the country’s technological advancements towards self-sufficiency in select industries.

- Undervalued cyclicals and consumer discretionary, particularly emerging local brands that are poised to benefit from China’s gradual macro stabilisation, improved margins from the execution of the anti-involution campaign, and stronger spending propensity supported by the positive wealth effect from the onshore equity market.

- Large banks and financials as reliable yield contributors that are able to consistently deliver stable and compelling dividends, offering attractive yields relative to China’s low deposit rate environment.

We also see investment opportunities in non-bank financials, stock exchanges, and industrials. The first two stand to benefit from a structural pickup in the onshore equity market and liquidity flows, while industrials are likely to ride on stabilising output costs and an improving profitability outlook as onshore competitive pressures ease.

There is ample room for China equities to re-rate as investment funds rotate into under-owned and attractively priced markets, supported by secular trends. As investors recalibrate their investments in an uncertain world, the potential for China equities becomes even more compelling.

We advocate maintaining an overweight position in China equities, with a focus on sectors poised for strong performance, including new economy, technology, platform companies, undervalued cyclicals, and those positioned to benefit from a resurgence in consumer spending. Timely and well-calibrated regulatory interventions should progressively reduce unwanted market volatility and enhance market investability, facilitating the reallocation of both investment funds and household wealth into the equity market, thereby driving a structural rally.

Figure 1: Dividend Per Share (DPS) continued to rise despite macro headwinds

Source: Bloomberg, DBS

Download the PDF to read the full report.

Topic

Explore more

CIO PerspectivesThis information herein is published by DBS Bank Ltd. (“DBS Bank”) and is for information only. This publication is intended for DBS Bank and its subsidiaries or affiliates (collectively “DBS”) and clients to whom it has been delivered and may not be reproduced, transmitted or communicated to any other person without the prior written permission of DBS Bank.

This publication is not and does not constitute or form part of any offer, recommendation, invitation or solicitation to you to subscribe to or to enter into any transaction as described, nor is it calculated to invite or permit the making of offers to the public to subscribe to or enter into any transaction for cash or other consideration and should not be viewed as such.

The information herein may be incomplete or condensed and it may not include a number of terms and provisions nor does it identify or define all or any of the risks associated to any actual transaction. Any terms, conditions and opinions contained herein may have been obtained from various sources and neither DBS nor any of their respective directors or employees (collectively the “DBS Group”) make any warranty, expressed or implied, as to its accuracy or completeness and thus assume no responsibility of it. The information herein may be subject to further revision, verification and updating and DBS Group undertakes no responsibility thereof.

All figures and amounts stated are for illustration purposes only and shall not bind DBS Group. This publication does not have regard to the specific investment objectives, financial situation or particular needs of any specific person. Before entering into any transaction to purchase any product mentioned in this publication, you should take steps to ensure that you understand the transaction and has made an independent assessment of the appropriateness of the transaction in light of your own objectives and circumstances. In particular, you should read all the relevant documentation pertaining to the product and may wish to seek advice from a financial or other professional adviser or make such independent investigations as you consider necessary or appropriate for such purposes. If you choose not to do so, you should consider carefully whether any product mentioned in this publication is suitable for you. DBS Group does not act as an adviser and assumes no fiduciary responsibility or liability for any consequences, financial or otherwise, arising from any arrangement or entrance into any transaction in reliance on the information contained herein. In order to build your own independent analysis of any transaction and its consequences, you should consult your own independent financial, accounting, tax, legal or other competent professional advisors as you deem appropriate to ensure that any assessment you make is suitable for you in light of your own financial, accounting, tax, and legal constraints and objectives without relying in any way on DBS Group or any position which DBS Group might have expressed in this document or orally to you in the discussion.

Any information relating to past performance, or any future forecast based on past performance or other assumptions, is not necessarily a reliable indicator of future results.

The information contained in this article has been obtained from sources believed to be reliable, but DBS makes no representation or warranty as to its adequacy, completeness, accuracy or timeliness for any particular purpose.

If this publication has been distributed by electronic transmission, such as e-mail, then such transmission cannot be guaranteed to be secure or error-free as information could be intercepted, corrupted, lost, destroyed, arrive late or incomplete, or contain viruses. The sender therefore does not accept liability for any errors or omissions in the contents of the Information, which may arise as a result of electronic transmission. If verification is required, please request for a hard-copy version.

This publication is not directed to, or intended for distribution to or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or other jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation.

If you have received this communication by email, please do not distribute or copy this email. If you believe that you have received this e-mail in error, please inform the sender or contact us immediately. DBS Group reserves the right to monitor and record electronic and telephone communications made by or to its personnel for regulatory or operational purposes. The security, accuracy and timeliness of electronic communications cannot be assured.

Please refer to the Additional Terms and Conditions Governing Digital Tokens for DBS Treasures Customers for more specific risk disclosures on trading of digital tokens.

This information does not constitute or form part of any offer, recommendation, invitation or solicitation to subscribe to or enter into any transaction. It does not have regard to your specific investment objectives, financial situation or particular needs. It is not intended to provide, and should not be relied upon for accounting, legal or tax advice.

Cryptocurrency trading is highly risky and prices can be very volatile. All investments come with risks and you can lose your entire investment. Before you decide to purchase an investment product, you should read all the relevant documents and carefully assess if it is suitable for you. Invest only if you understand and can monitor your investmen. Diversify your investments and avoid investing a large portion of your money in a single asset type.

Trading in Cryptocurrencies or the instrument (“Instrument”), such as ETF, referencing or with underlying as Cryptocurrencies ("Crypto-Products”), such as Bitcoin ETFs, is highly risky and prices can be very volatile. All investments come with risks and you can lose your entire investment. By trading in Crypto-Products, you are exposed to the risks of both the Instrument and the Cryptocurrencies. Further, Crypto-Products listed on overseas exchanges may not be regulated in Singapore, and are subject to the laws and regulations of the jurisdiction it is listed in. Before you decide to buy or sell Cryptocurrencies or Crypto-Products, you should read all the relevant documents and carefully assess if it is suitable for you and/or seek advice from a financial adviser regarding its suitability. Invest only if you understand and can monitor your investment. Diversify your investments and avoid investing a large portion of your money in a single asset type.

To the extent permitted by law, DBS accepts no liability whatsoever for any direct, indirect or consequential losses or damages arising from or in connection with the use or reliance of this email or its contents. If this information has been distributed by electronic transmission, such as e-mail, then such transmission cannot be guaranteed to be secure or error-free as information could be intercepted, corrupted, lost, destroyed, arrive late or incomplete, or contain viruses.

Please refer to Terms and Conditions governing your banking relationship with DBS for more specific risk disclosures on the Instrument (such as ETFs under Funds) and Digital Tokens.

This information is provided to you as an “Accredited Investor” (defined under the Securities and Futures Act of Singapore and the Securities and Futures (Classes of Investors) Regulations 2018) for your private use only. It is not intended for distribution to, or use by, any person or entity in any jurisdiction or country where such distribution or use would be contrary to law or regulation, and may not be passed on or disclosed to any person nor copied or reproduced in any manner.

DBS (Company Registration. No. 196800306E) is an Exempt Financial Adviser as defined in the Financial Advisers Act and regulated by the Monetary Authority of Singapore (the "MAS")

Related Insights

- DBS Stock Pulse: (1) Global Technology - Nvidia’s USD5bn bet accelerates Intel’s turnaround (2) Hongkong Land - Punching above SGD7 amid value unlocking progress19 Sep 2025

- DBS Stock Pulse: (1) Market view - 3 implications from the Fed’s measured cut (2) Global Technology Stocks - 7 stocks to watch as China accelerates its self-reliance agenda (3) Equity Picks: Remove Keppel REIT from Dividend18 Sep 2025

- Equities Weekly: European Banks – Beneficiaries of a Steepening Yield Curve17 Sep 2025

Related Insights

- DBS Stock Pulse: (1) Global Technology - Nvidia’s USD5bn bet accelerates Intel’s turnaround (2) Hongkong Land - Punching above SGD7 amid value unlocking progress19 Sep 2025

- DBS Stock Pulse: (1) Market view - 3 implications from the Fed’s measured cut (2) Global Technology Stocks - 7 stocks to watch as China accelerates its self-reliance agenda (3) Equity Picks: Remove Keppel REIT from Dividend18 Sep 2025

- Equities Weekly: European Banks – Beneficiaries of a Steepening Yield Curve17 Sep 2025