- Banking

- Wealth

- NRI Banking

- Customer Services

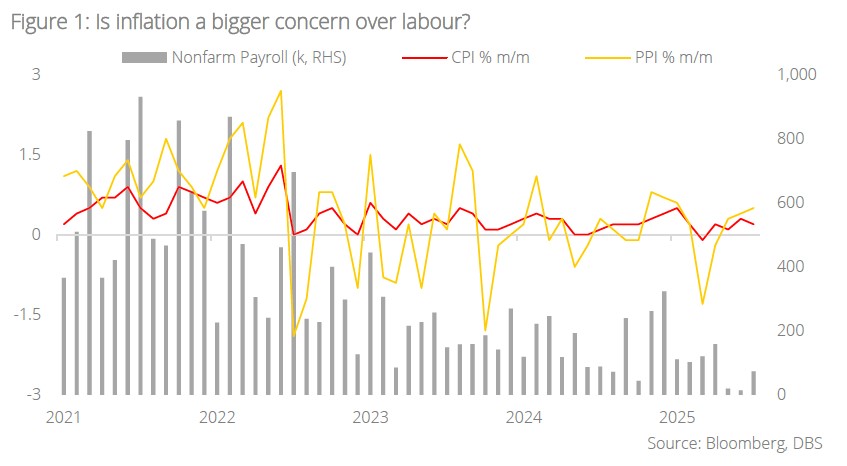

- US: Most Fed officials now fear tariff-driven inflation more than job market weakness; all eyes are on Powell's Jackson Hole speech for the next move

- China: July’s data prints signalled an excess supply driven slowdown in 2025; firms are expected to scale back production amid “anti-volution” campaign

- Thailand: After resilient 2Q25 GDP growth, we see lower growth in 2H25 due to weak exports, subdued foreign tourism, and sluggish investments

- Indonesia: BI reduced rates to 5%, affirming our off-consensus call; as the Fed embarks on its easing cycle in September, we expect BI to cut by another 25 bps in 4Q25

Related Insights

- Market Pulse: Dovish Fed25 Aug 2025

- CIO Market Pulse – Trifecta Boost18 Aug 2025

- Market Pulse: Trifecta Boost18 Aug 2025

US: Powell’s balancing act at Jackson Hole. The 30 Jul FOMC Minutes showed most Fed officials viewed the tariff passthrough into inflation as the bigger risk than weak jobs. However, at the time, Fed officials were handed a stronger-than-expected June nonfarm payroll print of 147k, later revised down sharply to just 14k with the unemployment rate rising back to 4.2% in July after a dip to 4.1% in June.

Meanwhile, US President Donald Trump is pressing ahead with efforts to reshape the seven-member Fed’s Board of Governors to align with his easing agenda. Two of his appointees, Michelle Bowman and Christopher Waller, had voted for a rate cut on 30 Jul. Having nominated Stephen Miran to replace Adriana Kugler, who surprisingly resigned on 8 Aug before her term expired in Jan 2026, Trump has called for Lisa Cook’s resignation over allegations of mortgage fraud. While Cook indicated no intention to be bullied into leaving the Fed, Federal Housing Financing Agency Director Bill Pulte will likely proceed to urge Attorney General Pam Bondi to investigate the matter.

The minutes suggest that most Fed officials will rally behind Powell’s cautious, data-dependent approach in lowering rates. Global central bankers attending Jackson Hole will likely emphasise that the credibility behind controlling inflation hinges on upholding central bank independence.

However, Powell may acknowledge sharply weaker jobs data released after the July meeting. In his 7 May post-FOMC press conference, Powell said that if unemployment increased in an uncomfortable manner, the Fed would look past supply-side inflation and lean towards supporting the labour market. By re-emphasising this contingency, Powell can maintain his inflation message while leaving the door open for the September cut that is already priced in by markets and potentially for more than one rate reduction if the labour market continues to deteriorate amid limited price pass-through from producers to consumers.

Download the PDF to read the full report which includes coverage on Credit, FX, Rates, and Thematics.

Topic

The information published by DBS Bank Ltd. (company registration no.: 196800306E) (“DBS”) is for information only. It is based on information or opinions obtained from sources believed to be reliable (but which have not been independently verified by DBS, its related companies and affiliates (“DBS Group”)) and to the maximum extent permitted by law, DBS Group does not make any representation or warranty (express or implied) as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions and estimates are subject to change without notice. The publication and distribution of the information does not constitute nor does it imply any form of endorsement by DBS Group of any person, entity, services or products described or appearing in the information. Any past performance, projection, forecast or simulation of results is not necessarily indicative of the future or likely performance of any investment or securities. Foreign exchange transactions involve risks. You should note that fluctuations in foreign exchange rates may result in losses. You may wish to seek your own independent financial, tax, or legal advice or make such independent investigations as you consider necessary or appropriate.

The information published is not and does not constitute or form part of any offer, recommendation, invitation or solicitation to subscribe to or to enter into any transaction; nor is it calculated to invite, nor does it permit the making of offers to the public to subscribe to or enter into any transaction in any jurisdiction or country in which such offer, recommendation, invitation or solicitation is not authorised or to any person to whom it is unlawful to make such offer, recommendation, invitation or solicitation or where such offer, recommendation, invitation or solicitation would be contrary to law or regulation or which would subject DBS Group to any registration requirement within such jurisdiction or country, and should not be viewed as such. Without prejudice to the generality of the foregoing, the information, services or products described or appearing in the information are not specifically intended for or specifically targeted at the public in any specific jurisdiction.

The information is the property of DBS and is protected by applicable intellectual property laws. No reproduction, transmission, sale, distribution, publication, broadcast, circulation, modification, dissemination, or commercial exploitation such information in any manner (including electronic, print or other media now known or hereafter developed) is permitted.

DBS Group and its respective directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned and may also perform or seek to perform broking, investment banking and other banking or financial services to any persons or entities mentioned.

To the maximum extent permitted by law, DBS Group accepts no liability for any losses or damages (including direct, special, indirect, consequential, incidental or loss of profits) of any kind arising from or in connection with any reliance and/or use of the information (including any error, omission or misstatement, negligent or otherwise) or further communication, even if DBS Group has been advised of the possibility thereof.

The information is not intended for distribution to, or use by, any person or entity in any jurisdiction or country where such distribution or use would be contrary to law or regulation. The information is distributed (a) in Singapore, by DBS Bank Ltd.; (b) in China, by DBS Bank (China) Ltd; (c) in Hong Kong, by DBS Bank (Hong Kong) Limited; (d) in Taiwan, by DBS Bank (Taiwan) Ltd; (e) in Indonesia, by PT DBS Indonesia; and (f) in India, by DBS Bank Ltd, Mumbai Branch.

Related Insights

- Market Pulse: Dovish Fed25 Aug 2025

- CIO Market Pulse – Trifecta Boost18 Aug 2025

- Market Pulse: Trifecta Boost18 Aug 2025

Related Insights

- Market Pulse: Dovish Fed25 Aug 2025

- CIO Market Pulse – Trifecta Boost18 Aug 2025

- Market Pulse: Trifecta Boost18 Aug 2025