Wealth Solutions

We save you the extensive research by partnering with reputed firms to bring you the best choice of wealth solutions.

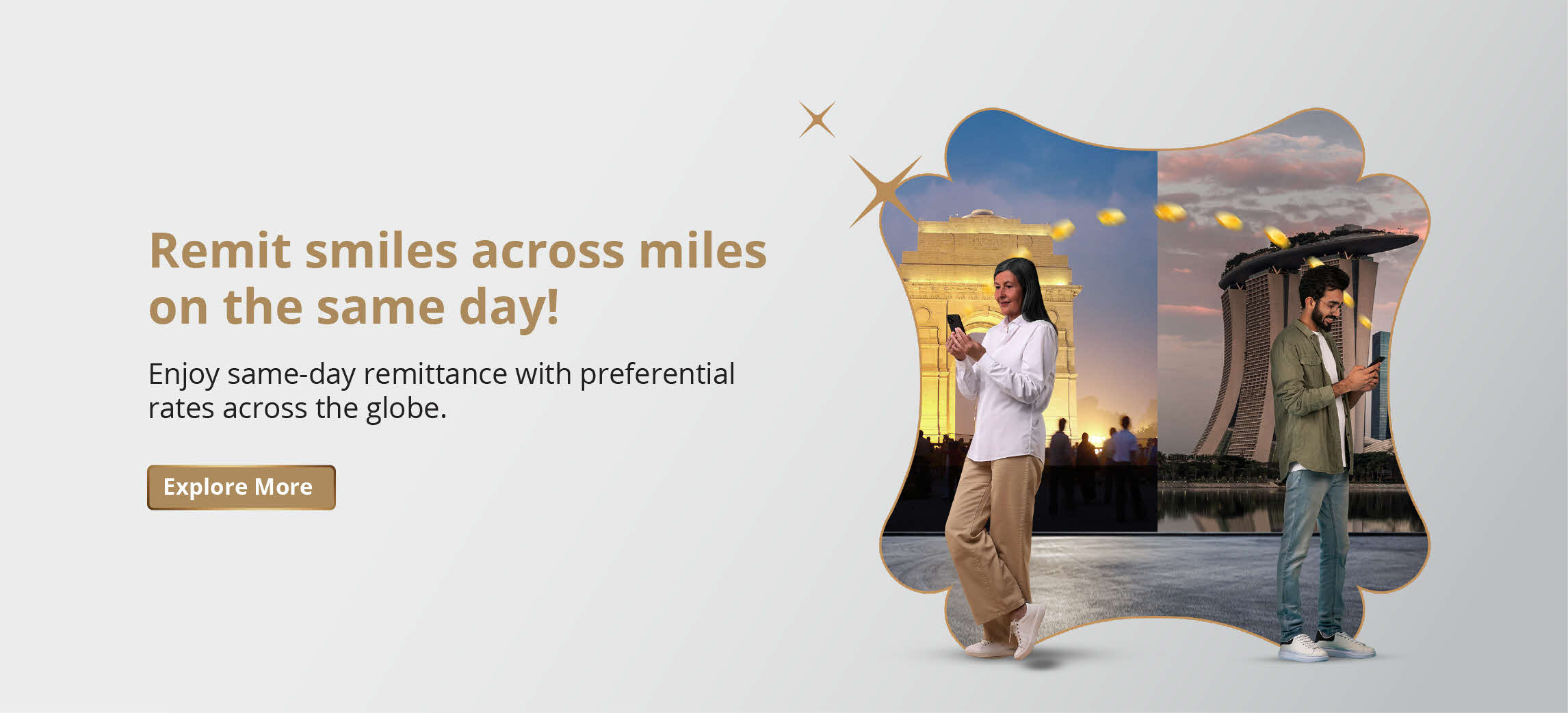

Imagine a banking experience that not only meets your needs, but exceeds them. Welcome to DBS Treasures, a personalized premium banking and wealth management program designed for those who seek the very finest in life. Enjoy banking, wealth management, lifestyle, travel, and health privileges that are unparallelled. Experience a world where Banking is Elevated.

DBS Treasures

NRI Banking

Treasures International

Remittance

Fixed Deposits

We save you the extensive research by partnering with reputed firms to bring you the best choice of wealth solutions.

Want to stay one step ahead of the curve? Our latest insights from Indian and international markets have got your back!

Enjoy a host of privileges that truly match your lifestyle and aspirations

(Total Relationship Value of INR ₹ 30L to INR ₹ 1Cr)

Step into a world of privileges. Discover premium privileges like:

(Total Relationship Value of INR ₹ 1Cr to INR ₹ 2Cr)

Where greater achievements meet richer rewards. Get access to exclusive privileges like:

(Total Relationship Value of INR ₹ 2Cr to INR ₹ 6Cr)

The finest experiences, reserved for the select few. Indulge in unparalleled privileges like:

*DBS Treasures is a premium banking proposition where the minimum relationship value with DBS Bank India Limited needs to be built up to INR 30 Lacs. The Total Relationship Value (TRV) is across all accounts in a family and calculated by aggregating average quarterly savings account balances and end of period term deposits, insurance, investments and mortgage loan outstanding. 40% of the net balance of the loan (Home Loan / LAP) will be considered towards TRV computation.

Signature lifestyle privileges, exclusive offers, unlimited ATM withdrawals and lowest forex mark-up on international spends

Your digital banking partner for managing your finances and your wealth, all by yourself

Learn more about our products & services and know what our customers have to say about us

DBS Treasures International

DBS Study Abroad Total Assist

DBS Golden Circle

Treasures Customer Testimonial