- Banking

- Wealth

- Privileges

- NRI Banking

- Treasures Private Client

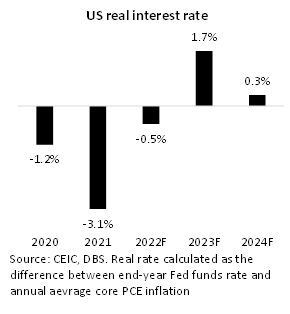

- We forecast US short-term real interest rates to go from -0.5% at end-2022 to +1.7% at end-2023

- Rising real rates will hurt home affordability and corporate profitability

- Some impact on labour markets and consumption is inevitable

- The balance of risk is not overwhelmingly one-sided

- Both inflation and growth could prove to be sticky, which would be major headwinds for markets

Related Insights

- Research Library26 Apr 2024

- China chartbook: 2Q24 GDP growth tracking 5%25 Apr 2024

- Bank Indonesia’s proactive hike 24 Apr 2024

Commentary: The year of rising (real) rates

After a year of historic rate increases, 2023 will test the ability of US households and companies to absorb a prolonged period of high interest rates. We expect the Fed funds rate to reach 5% by the end of the first quarter, and then the policy rate to remain unchanged till end 2023. This is largely consistent with the median forecast of the members of the Federal Reserve’s Open Market Committee. It is widely expected that supply and demand conditions are aligned for inflation to decline next year, but not to the extent to make the monetary authorities comfortable enough to begin cutting rates. That would have to wait till the first quarter of 2024, in our view.

As we expect a gradual decline in price pressures through the course of the year, this would imply a substantial rise in real interest rates. As per our forecasts, short-term real interest rates, calculated as end-period Fed funds rate minus average core personal consumption expenditure inflation, will go from -0.5% at end-2022 to +1.7% at end-2023.

Will credit growth for personal and business spending and mortgage financing sustain under the envisaged 220bps of real interest rate increases within a year? We are doubtful. Such high rates are bound to erode home affordability, reduce corporate profitability, and impose pressure on firms to reduce employment. The labour market, still buoyant despite the outsized rate increases of this year, will eventually feel the pinch. We expect to see unemployment rise from 3.5% to 4.5% in 2023.

There is a good chance the recent trend softening seen in the cost of shipping, manufactured goods, energy, and food will persist, helping keep inflation on a downward trajectory, which is a major positive in the making for the global economy.

Global fixed income markets are pricing in that the monetary policy cycle is not only close to peak, but rates will be heading down in less than a year. These predictions are predicated on inflation and economic growth slowing substantially this year. We also expect both, but recognise that the balance of risk is not overwhelmingly one-sided. Inflation may well prove to be stickier, as could growth, as seen by US jobs and sales numbers in recent months.

Rising rates have already had a chilling impact on home prices; rents, and their contribution to inflation, are about follow. The job market ought to be the next shoe to drop, with the downsizing trend already seen in the tech sector spread to a wider set of sectors. That in turn should have a sobering impact on wages.

But it would be premature to ignore a scenario under which jobs, wages, and prices don’t weaken sufficiently and swiftly enough for the market’s expectation of a late 2023 rate cut cycle to materialise. Household and corporare debt ratios are low by historical standards, which could set the ground for surprising resiliency. That would put the Fed in quandary, as it faces weakening growth and yet to need to hold on to its policy leash. 2023 may well be the ultimate test of Fed credibility.

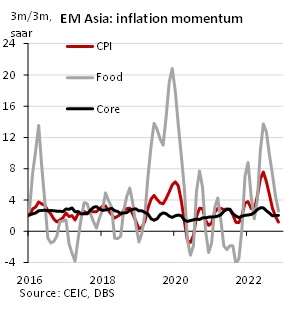

What does all this mean for Asia? With the exception of China, Asian economies were compelled to normalise monetary policy in 2022, pulled by the Fed’s actions. Inflation momentum has eased substantially in the region in recent months, but that doesn’t mean the room to ease policy is opening up. Even as growth slows, Asian policy makers would prefer to keep rates above the historically low rates seen during the pandemic. This would hold in particular if the year’s slowdown is driven by weak external demand, in our view.

Taimur Baig

To read the full report, click here to Download the PDF.

Topic

The information herein is published by DBS Bank Ltd and/or DBS Bank (Hong Kong) Limited (each and/or collectively, the “Company”). This report is intended for “Accredited Investors” and “Institutional Investors” (defined under the Financial Advisers Act and Securities and Futures Act of Singapore, and their subsidiary legislation), as well as “Professional Investors” (defined under the Securities and Futures Ordinance of Hong Kong) only. It is based on information obtained from sources believed to be reliable, but the Company does not make any representation or warranty, express or implied, as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions expressed are subject to change without notice. This research is prepared for general circulation. Any recommendation contained herein does not have regard to the specific investment objectives, financial situation and the particular needs of any specific addressee. The information herein is published for the information of addressees only and is not to be taken in substitution for the exercise of judgement by addressees, who should obtain separate legal or financial advice. The Company, or any of its related companies or any individuals connected with the group accepts no liability for any direct, special, indirect, consequential, incidental damages or any other loss or damages of any kind arising from any use of the information herein (including any error, omission or misstatement herein, negligent or otherwise) or further communication thereof, even if the Company or any other person has been advised of the possibility thereof. The information herein is not to be construed as an offer or a solicitation of an offer to buy or sell any securities, futures, options or other financial instruments or to provide any investment advice or services. The Company and its associates, their directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned herein and may also perform or seek to perform broking, investment banking and other banking or financial services for these companies. The information herein is not directed to, or intended for distribution to or use by, any person or entity that is a citizen or resident of or located in any locality, state, country, or other jurisdiction (including but not limited to citizens or residents of the United States of America) where such distribution, publication, availability or use would be contrary to law or regulation. The information is not an offer to sell or the solicitation of an offer to buy any security in any jurisdiction (including but not limited to the United States of America) where such an offer or solicitation would be contrary to law or regulation.

This report is distributed in Singapore by DBS Bank Ltd (Company Regn. No. 196800306E) which is Exempt Financial Advisers as defined in the Financial Advisers Act and regulated by the Monetary Authority of Singapore. DBS Bank Ltd may distribute reports produced by its respective foreign entities, affiliates or other foreign research houses pursuant to an arrangement under Regulation 32C of the Financial Advisers Regulations. Singapore recipients should contact DBS Bank Ltd at 65-6878-8888 for matters arising from, or in connection with the report.

DBS Bank Ltd., 12 Marina Boulevard, Marina Bay Financial Centre Tower 3, Singapore 018982. Tel: 65-6878-8888. Company Registration No. 196800306E.

DBS Bank Ltd., Hong Kong Branch, a company incorporated in Singapore with limited liability. 18th Floor, The Center, 99 Queen’s Road Central, Central, Hong Kong SAR.

DBS Bank (Hong Kong) Limited, a company incorporated in Hong Kong with limited liability. 13th Floor One Island East, 18 Westlands Road, Quarry Bay, Hong Kong SAR

Virtual currencies are highly speculative digital "virtual commodities", and are not currencies. It is not a financial product approved by the Taiwan Financial Supervisory Commission, and the safeguards of the existing investor protection regime does not apply. The prices of virtual currencies may fluctuate greatly, and the investment risk is high. Before engaging in such transactions, the investor should carefully assess the risks, and seek its own independent advice.

Related Insights

- Research Library26 Apr 2024

- China chartbook: 2Q24 GDP growth tracking 5%25 Apr 2024

- Bank Indonesia’s proactive hike 24 Apr 2024

Related Insights

- Research Library26 Apr 2024

- China chartbook: 2Q24 GDP growth tracking 5%25 Apr 2024

- Bank Indonesia’s proactive hike 24 Apr 2024