- Banking

- Wealth

- Privileges

- NRI Banking

- Treasures Private Client

- Equities: Bank run on SVB triggered broad-based market weakness; no systemic fallout expected

- Credit: Amid fears of rampant risk, high quality, short duration credit minimises exposure to risk

- FX: USD to soften before Fed meeting on 22 Mar; UK budget to underpin GBP within 3-month range

- Rates: Financial stability concerns to outweigh inflation worries for the Fed

- Thematics: Lithium consumption growth in power storage and battery production set to remain strong

No systemic fallout from SVB debacle. Broad-based market weakness amid second largest bank failure in US history. Stocks plummeted last week (ended 10 March) as risk sentiment took a big hit from Silicon Valley Bank’s (SVB) failed equity raise and subsequent bank run on Thursday (9 March). Global equities were down 3.6%, with Developed Markets and Emerging Markets falling 3.6% and 3.3% respectively.

US equities reversed their gains from the week before and notched one of their largest weekly losses of the year. The S&P 500, NASDAQ, and Dow fell 4.6%, 4.7%, and 4.4% respectively. The Dow’s decline was the largest since June 2022. Europe also fell amid the SVB plunge; the FTSE 100 and Stoxx 600 dipped 2.5% and 2.3% for the week. Asian equities were mixed with Hong Kong and China tumbling while Japan equities logged modest gains; HSCEI and Hang Seng were down 7.1% and 6.1%, while Nikkei 225 rose 0.8% for the week.

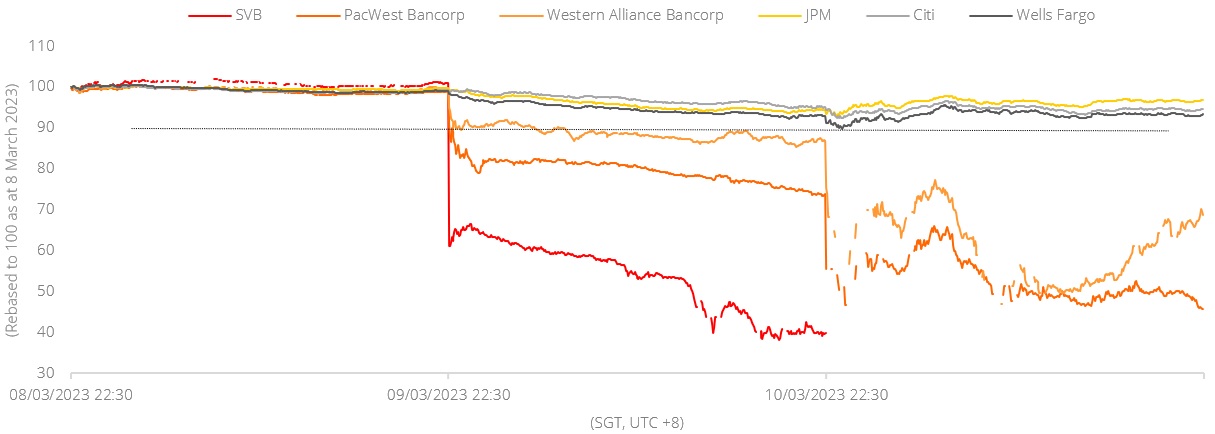

Topic in focus: No systemic fallout from SVB debacle; seek resilience from quality names. Notwithstanding the sizeable selloff, we believe that SVB’s collapse will not have significant contagion effect on the broader market as the incident was caused by the unique composition of SVB’s balance sheet rather than a systemic liquidity risk. To be specific, SVB held a large proportion of its assets in investments (57%) compared to the average US bank (24%), and it is this outsized exposure to interest rate-sensitive instruments coupled with the lack of hedging measures that contributed to the erosion of its asset base and subsequent need for fundraising. These circumstances were specific to SVB, and its share price performance reflected that; as can be seen in Figure 1, the share price of niche financial companies, including SVB, fell more than large banks such as JPM, Citi, and Wells Fargo.

This incident reinforces our preference for quality as companies with established track records, robust financials, and strong economic moats are better able to withstand market shake-ups. Our strategies to navigate the current environment are as follows:

- Stick with quality for growth equities and favour investment grade credit over high yield

- Gain exposure to alternatives such as gold and private assets to create a holistic and resilient portfolio construct

Figure 1: Major US banks were largely spared from the selloff

Source: Bloomberg, DBS

Topic

This information herein is published by DBS Bank Ltd. (“DBS Bank”) and is for information only. This publication is intended for DBS Bank and its subsidiaries or affiliates (collectively “DBS”) and clients to whom it has been delivered and may not be reproduced, transmitted or communicated to any other person without the prior written permission of DBS Bank.

This publication is not and does not constitute or form part of any offer, recommendation, invitation or solicitation to you to subscribe to or to enter into any transaction as described, nor is it calculated to invite or permit the making of offers to the public to subscribe to or enter into any transaction for cash or other consideration and should not be viewed as such.

The information herein may be incomplete or condensed and it may not include a number of terms and provisions nor does it identify or define all or any of the risks associated to any actual transaction. Any terms, conditions and opinions contained herein may have been obtained from various sources and neither DBS nor any of their respective directors or employees (collectively the “DBS Group”) make any warranty, expressed or implied, as to its accuracy or completeness and thus assume no responsibility of it. The information herein may be subject to further revision, verification and updating and DBS Group undertakes no responsibility thereof.

All figures and amounts stated are for illustration purposes only and shall not bind DBS Group. This publication does not have regard to the specific investment objectives, financial situation or particular needs of any specific person. Before entering into any transaction to purchase any product mentioned in this publication, you should take steps to ensure that you understand the transaction and has made an independent assessment of the appropriateness of the transaction in light of your own objectives and circumstances. In particular, you should read all the relevant documentation pertaining to the product and may wish to seek advice from a financial or other professional adviser or make such independent investigations as you consider necessary or appropriate for such purposes. If you choose not to do so, you should consider carefully whether any product mentioned in this publication is suitable for you. DBS Group does not act as an adviser and assumes no fiduciary responsibility or liability for any consequences, financial or otherwise, arising from any arrangement or entrance into any transaction in reliance on the information contained herein. In order to build your own independent analysis of any transaction and its consequences, you should consult your own independent financial, accounting, tax, legal or other competent professional advisors as you deem appropriate to ensure that any assessment you make is suitable for you in light of your own financial, accounting, tax, and legal constraints and objectives without relying in any way on DBS Group or any position which DBS Group might have expressed in this document or orally to you in the discussion.

Any information relating to past performance, or any future forecast based on past performance or other assumptions, is not necessarily a reliable indicator of future results.

If this publication has been distributed by electronic transmission, such as e-mail, then such transmission cannot be guaranteed to be secure or error-free as information could be intercepted, corrupted, lost, destroyed, arrive late or incomplete, or contain viruses. The sender therefore does not accept liability for any errors or omissions in the contents of the Information, which may arise as a result of electronic transmission. If verification is required, please request for a hard-copy version.

This publication is not directed to, or intended for distribution to or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or other jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation.

If you have received this communication by email, please do not distribute or copy this email. If you believe that you have received this e-mail in error, please inform the sender or contact us immediately. DBS Group reserves the right to monitor and record electronic and telephone communications made by or to its personnel for regulatory or operational purposes. The security, accuracy and timeliness of electronic communications cannot be assured.