3Q25 Key Investment Takeaways: The Global Pivot | Bahasa

- Macro Policy

Outside the US, stronger currencies vs the US dollar and a marked decline in commodity prices have muted inflation concerns. Despite the pause in US tariffs, tensions continue to simmer between the US and its trading partners.

- Economic Outlook

Oil prices surge due to Israel-Iran conflict, but our base-case sees limited second-order effects in the wider markets. The market is likely to shift its focus to the risk of inflation as the China-US trade war reprieve fades. We revise down Europe and Japan growth.

- Equities

Maintain high conviction calls on US tech as the AI trend persists. On a 3-month basis, overweight Europe and AxJ on resurgent fiscal impulse, favourable dividend yield, and valuation discount.

- Credit

Stagflation risks and long-end volatility have risen. Prioritise A/BBB while maintaining a barbell duration strategy, overweighting 2-3Y and 7-10Y segments. We like US Treasury Inflation-Protected Securities (TIPS), capital securities, and short duration quality credit.

- Rates

Bond vigilantes lurk as fiscal challenges deepen in the US and Japan. As investors look to diversify their holdings away from USD assets, a shift in capital flows benefit Asian local currency bonds

- Currencies

Weaker USD trajectory to continue as Trump’s controversial policy-making style has eroded confidence in USD assets. Alternative safe haven currencies will be primary beneficiaries.

- Alternatives

Favourable risk-reward in gold from central bank buying. Add hedge funds, private secondaries, credit, and private infrastructure for additional sources of alpha returns.

- Commodities

As the impact of tariff front-running subsidies and growth risks increase, sentiment and fund flows are likely to lean cautious for all commodity sub-sectors, with the exception of precious metals.

- Thematic focus: New World Order

We explore humanoids, industrial automation, and defence & aerospace as key beneficiaries in a world that is increasingly shaped by reshoring and self-reliance.

Trump's first 100 days delivered shock and awe, from aggressive DOGE cost cuts to unleashing a global tariff war. While his approach has repositioned America with far-reaching consequences, policy ambiguity remains an ongoing feature, increasing risk premiums for US financial assets. The recent passage of expansive tax reform has raised serious questions about debt sustainability, with CBO projections showing the budget deficit hitting USD1.9tn this year and federal debt reaching 118% of GDP by 2035. Moody's downgrade of the US credit rating to Aa1 symbolically marks the end of "risk-free" US Treasuries, while 30-year yields breaching 5% reflect growing unease over fiscal sustainability.

Trump's "beautiful tariff war" serves dual purposes: strategic containment of China and revenue generation to address America's insolvency. However, even aggressive 20% universal tariffs would generate only USD185.2bn in additional revenue after dynamic effects - barely covering debt interest payments.

This fiscal reality drives our key portfolio switches: (a) Maintain Neutral stance on equities while expecting divergence in performance across sectors and geographies; maintain conviction on US technology while services outperform goods-focused sectors; (b) Downgrade developed market (DM) government bonds to Neutral given fiscal concerns and sticky inflation; adopt duration barbell approach in credit; and (c) Overweight alternatives, particularly gold (target USD3,765/oz by 4Q25) and income-generating private assets.

Three key themes will dominate 3Q25: pragmatic de-escalation of tariff tensions, divergent equity performance, and fiscal headwinds which are negative for government bonds and the dollar but positive for gold. The abrupt de-escalation in US-China tensions has surprised markets, driven by pragmatism, as the 145% tariffs essentially constitute trade embargos that hurt both parties. With USD7.8tn of US debt requiring refinancing this year and waning poll numbers at home, Trump's embrace of progressive policies underlines efforts to reframe Republicans as the working-class party ahead of 2026 midterms.

Gold's traditional inverse relationship with bond yields has broken down since "Liberation Day", reflecting new dynamics around fiscal sustainability and de-dollarisation. Central bank gold demand hit 1,045 tonnes in 2024 (121% above the 2010–2021 historical average), suggesting persistent diversification away from US financial assets. Dollar weakness of -9.7% YTD despite surging Treasury yields reflects growing reservations about the greenback's reserve currency status.

In summary, US fiscal profligacy and policy ambiguity are increasing risk premiums across financial assets. While pragmatism will likely underpin tariff de-escalation, expect significant divergence in equity performance with technology and services outperforming. Our defensive shift maintains overweight alternatives - particularly gold and income-generating private assets - for essential portfolio resilience in this era of a global pivot from US financial asset dominance.

Key highlights of our tactical calls for the quarter are:

- Cross Assets – Bonds remain in play

Maintain preference for bonds over equities amid stagflationary backdrop. US manufacturing momentum has moderated since the start of the year while economic surprises disappoint as trade war uncertainties erode business confidence and deter corporate capex. Paradoxically, this growth slowdown is coinciding with upward inflation risks from supply chain disruptions, labour market tightness, and rising money supply growth, with companies already reporting sharp input cost increases. US earnings forecasts have been revised down marginally, suggesting analyst assumptions of trade de-escalation, with similar downtrends in Europe and Japan. Asia ex-Japan bucked the trend with expected FY2025 earnings growth of 12.4% (vs 6.6% for DMs).

- Equities – Maintain conviction on US Technology; Overweight Europe

Given prevailing tariff uncertainties, country allocation calls face binary outcomes depending on July trade deal negotiations. We maintain a base-case assumption of pragmatic de-escalation with China and Europe. Within DMs, maintain slight Underweight on US equities as consensus earnings forecasts remain overly optimistic at 11% (vs 7% for DMs) and dollar weakness compels portfolio diversification. However, Nvidia's strong guidance reinforces the resilience of the AI theme, with technology momentum expected to partially offset weaknesses in US non-tech sectors. Maintain Overweight on Europe given US fiscal sustainability concerns, which are driving allocation shifts, and resurgent defence spending. Asia ex-Japan remains a deep value play at 33% discount to DMs with 12.4% expected earnings growth.

- Bonds – Duration barbell approach amid fiscal and inflation concerns

Market attention has shifted to fiscal sustainability as long-term yields drift higher on demand-supply imbalances. Recent spikes in long-duration Treasuries and JGB yields reflect sticky inflation unlikely to subside given tariff uncertainties, labour market tightness, and money supply growth. On both a 3-month and 12-month basis, downgrade DM government bonds to Neutral as higher long-term yields and curve steepening are expected. In credit, stay with quality in the A/BBB bucket and adopt a duration barbell approach with 2-3Y and 7-10Y IG exposure. Our 2-3Y Liquid+ strategy remains well-positioned for stagflationary conditions. We remain less convinced on HY given spread-widening risks.

- Alternatives – Overweight Gold with target price of USD 3,765/oz by 4Q25; seek opportunities in income-generating private assets

Gold benefits either way in Trump 2.0. On one side of the equation, Trump’s taxation cuts and deregulation will only serve to exacerbate longer-term concerns of monetary debasement in the US. On the other end of the equation, the unleashing of trade tariffs and policy shocks will only drive bond yields lower and trigger the flight to safe havens like gold.

In private assets, we advise investors to seek opportunities in middle market buyouts and growth private equity. Middle market companies possess lower purchase multiples, providing room for larger future value expansion. Besides, the requirement for lower leverage in middle market deals auger well for their outlook in a high-interest rate environment.

[END]

Appendix

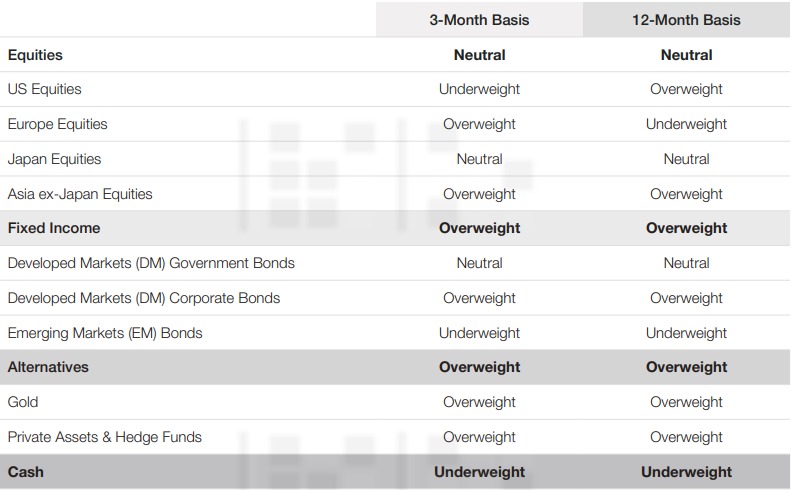

3Q25 CIO Asset Allocation (CIO AA)

Source: DBS

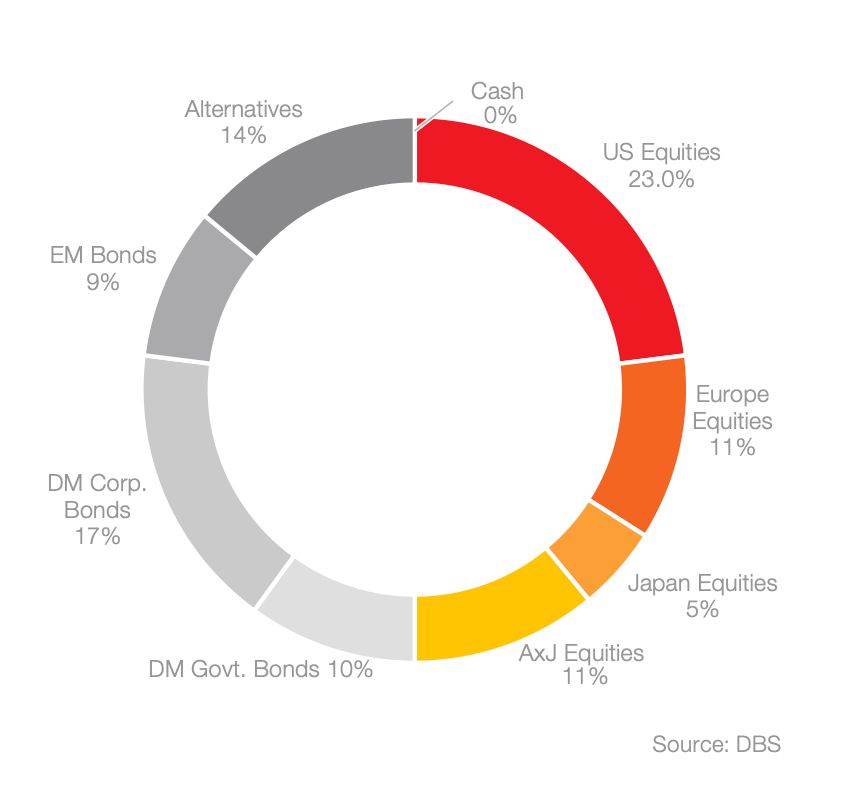

CIO AA Breakdown by Asset Class (Medium-Risk Profile)

Source: DBS

About DBS

DBS is a leading financial services group in Asia with a presence in 19 markets. Headquartered and listed in Singapore, DBS is in the three key Asian axes of growth: Greater China, Southeast Asia and South Asia. The bank's "AA-" and "Aa1" credit ratings are among the highest in the world.

Recognised for its global leadership, DBS has been named “World’s Best Bank” by Global Finance, “World’s Best Bank” by Euromoney and “Global Bank of the Year” by The Banker. The bank is at the forefront of leveraging digital technology to shape the future of banking, having been named “World’s Best Digital Bank” by Euromoney and the world’s “Most Innovative in Digital Banking” by The Banker. In addition, DBS has been accorded the “Safest Bank in Asia” award by Global Finance for 16 consecutive years from 2009 to 2024.

DBS provides a full range of services in consumer, SME and corporate banking. As a bank born and bred in Asia, DBS understands the intricacies of doing business in the region’s most dynamic markets.

Established in 1989 as part of the Singapore-based DBS Group, PT Bank DBS Indonesia (Bank DBS Indonesia) is one of the banks with the longest history in Asia. Currently operating 1 Head Office, 13 Branch Offices, 16 Assistant Offices and 1 Functional Office and 3,011 active employees in 15 Major Cities in Indonesia, Bank DBS Indonesia provides comprehensive banking services that focus on the customer experience to 'Live more, Bank less'. We also see a purpose beyond banking and are committed to supporting our customers, employees, and the community towards a sustainable future.

PT Bank DBS Indonesia is licensed and supervised by The Indonesian Financial Services Authority (OJK), and an insured member of Indonesia Deposit Insurance Corporation (LPS).

DBS is committed to building lasting relationships with customers, as it banks the Asian way. Through the DBS Foundation, the bank creates impact beyond banking by supporting businesses for impact: enterprises with a double bottom-line of profit and social and/or environmental impact. DBS Foundation also gives back to society in various ways, including equipping underserved communities with future-ready skills and helping them to build food resilience.

With its extensive network of operations in Asia and emphasis on engaging and empowering its staff, DBS presents exciting career opportunities. For more information, please visit www.dbs.com.

DBS Group

Useful Links

Awards

World's Best Bank 2025, 2018 - 2022

Euromoney, Global Finance, The Banker

Asia’s Safest Bank, 2009 – 2025

Global Finance