DBS Chief Investment Office 2Q26 Insights: Resilience in Chaos Key Investment Takeaways

First, the Middle East war and its impact on risk assets. Oil remains the key transmission channel of the military crisis, given Iran’s role as the fourth‑largest OPEC producer. The scale and duration of any oil price shock hinge on developments at the Strait of Hormuz, a critical chokepoint for global oil and LNG trade. Rising energy prices is problematic for risk assets as they raise inflation expectations, limit central bank’s scope for monetary easing, and weigh on economic growth.

Second, Warsh and the Fed narrative reset. Warsh’s policy stance signals a potential reset in the Federal Reserve’s narrative. He believes that AI-led production gains allow the Fed’s aggressive rate cuts without stoking inflation. At the same time, his concerns over “monetary dominance” led to his view of a significant reduction in the Fed’s balance sheet. This raises the likelihood of renewed quantitative tightening and implies yield curve steepening, a dynamic that is supportive for financials.

Last, diversification beyond crowded trades. Geopolitical tensions have disrupted markets, triggering profit‑taking in recent winners such as Korea and Japan. We view this as transitory. As the volatility subsides, we expect investors to return to fundamentals and re-focus with dominant pre-crisis themes –notably precious metals and technology– driven by as “dollar debasement” and “AI supremacy”, respectively. We advocate investors to diversify away from crowded trades and recommend adding exposure to Emerging Markets (EM) equities and Japan equities. EM equities stand to benefit from Fed rate cuts, dollar weakness, strong earnings growth, and light positioning; while Japan equities are supported by forthcoming fiscal stimulus, governance reforms and attractive yield gap.

Key tactical call highlights

Cross Assets: Fair Game

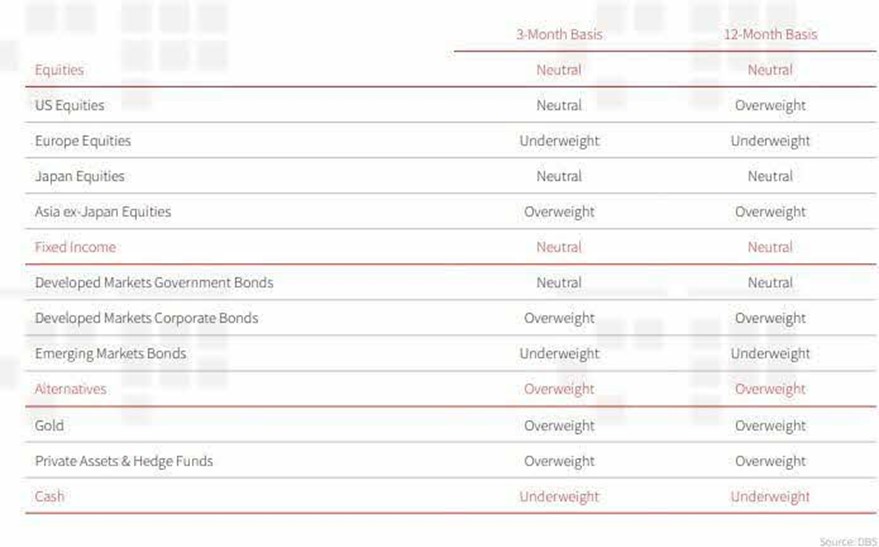

We adopt a broadly neutral stance across asset classes. The US economy, while resilient, is showing early signs of moderation, as evidenced by retail sales numbers. This coincides with the recent downward revision of Atlanta Fed GDPNow’s GDP forecast from c.5% to c.3%. But despite this slight slowdown, barring no adverse spill-over effects from the Middle East war, we do not foresee a recession this year, as macro momentum stays underpinned by the AI capex cycle and Trump’s fiscal stimulus. Global corporate earnings are projected to grow about 17% in 2026. Bonds appear more attractively valued than equities. Fund inflows into both equities and bonds have strengthened marginally relative to 2025. Flow momentum into US equities has declined substantially, while the likes of Europe and Japan have registered stronger momentum, underpinning our view of an ongoing portfolio rotation away from the US.

Equities: Maintain conviction view on Asia ex-Japan; upgrade Japan to neutral

Asia ex-Japan (AxJ) equities have outperformed developed markets this year amid (1) de-escalation of trade tension and (2) portfolio rotation away from crowded trades in the US. But despite the outperformance, AxJ continues to trade at substantial discount to DM equities given its superior earnings growth momentum. We expect the outperformance for AxJ to persist as investors seek to reduce exposure to US-based assets and ride on the AI capex boom in Asia. We have also upgraded our view on Japan equities, expecting the market to grind higher, given narrowing of valuation discounts alongside corporate governance reforms, attractive yield gap vs. domestic government bonds, and ongoing structural reforms as evidenced by rising dividend payout and corporate share buybacks. We favour Japan’s winning sectors that are poised to benefit from Takaichi’s strategy.

Bonds: Switch bonds to neutral; maintain overweight on IG

While we maintain our preference for quality in the A/BBB segment, we are also cognisant that not all industries will perform equally in the era of AI anxiety and divergence. The acute sell-down of software equities may serve as, perhaps, a canary in the coal mine for credit markets. Given the threat of potential business obsolescence arising from AI disruption, some industries or companies with investment-grade (IG) ratings will no longer be regarded as safe havens. In this environment, cyclical sectors that are “capital heavy” may paradoxically be safer havens as compared to “capital light” ones. Given tight spreads and AI-related headwinds, spread compression will be more muted. We maintain our preference for short duration (2-3 year), high quality credit, and portfolio duration of 5-7 years. While we stay positive on IG credit, we are paring down our overweight stance moderately, bringing our overall bond allocation to neutral.

Alternatives: Positive on gold and hedge funds

Gold’s sharp sell-down following Trump’s nomination of Warsh as Fed Chair proved transitory, as the precious metal reasserted itself as a dominant portfolio diversifier and resumed its uptrend. In an era of geopolitical uncertainties, we see no other precious metals as a viable alternative to gold, which continues to be underpinned by dollar debasement concerns, geopolitical risks, and strong central bank demand. We have raised our 2H26 target price to USD6,250/oz. Recent volatility in software companies also highlights the importance of hedge fund exposure in a portfolio construction as long/short managers are able to put in short positions and reap substantial upsides. We believe hedge fund strategies like macro, relative value, and long/short equity are well-positioned to navigate AI-driven disruptions.

2Q26 Investment Summary

Macro

- US

Rising downside risks to consumption - from potential equity market weakness, tariff driven inflation, job uncertainty, and oil price shocks — alongside political pressure and the Fed’s willingness to run the economy “hot” despite above-target inflation underpin our call for two insurance rate cuts in 3Q and 4Q.

- Eurozone

We upgrade 2026 GDP growth projection, following the region’s robust broad recovery at 2025-end. Prioritisation of domestic strategic autonomy, easing financial conditions, and Germany’s fiscal spending, specifically toward defence and infrastructure, should anchor outlook.

- Japan

Following a supermajority election victory, PM Takaichi’s substantial latitude to enact bills with limited resistance positions fiscal expansion at the top of the agenda with her push for strategic sector investments. We expect BOJ to continue with policy normalisation.

- Asia

China’s economy is growing at a slower pace but towards domestic consumption and investment. India and ASEAN outlooks remain robust, underpinned by supportive fiscal policies. Asia’s investment and exports should continue to benefit from global AI-related expenditure.

- US

Maintain neutral stance as concerns loom over dollar assets and crowded technology exposure. Market's initial focus on innovators is shifting to the identification of winners and losers of the AI revolution. We are positive on the AI infrastructure plays of utilities and energy.

- Europe

Relative near-term performance may lag in favour of Asia, which feature more compelling earnings momentum and policy optionality. Remain constructive on selective sectors of industrials, utilities, tech, and healthcare.

- Japan

Following Takaichi’s supermajority victory, investor attention will pivot towards pro-growth, reflationary policies through calibrated fiscal expansion. Corporate reform should support further re-rating despite rich valuations. Stay constructive on structural winners.

- Asia ex-Japan

Asia ex-Japan equities offer attractive valuations and robust earnings outlook, driven by technology and AI. The region’s declining energy intensity buffers against oil shocks. China anchors the recovery, while Singapore offers attractive dividend plays.

- Investment Grade

IG credit remains supported by strong balance sheets and structural demand for high-quality income as safe assets dwindle. However, AI-driven capex, tighter spreads, and fading policy tailwinds limit upside. Stay up in quality (A/BBB) with overall portfolio duration of 5-7Y..

- High Yield

HY credit offers limited compensation for rising risks as tight spreads, fading policy support, and AI-driven disruption leave little margin for error. With refinancing risks mounting and rates potentially staying higher, we favour restrained exposure and an up-in-quality stance.

- Global

The mix of US economic resilience and upside risks to inflation stemming from the Middle East conflict means that the Fed will be on hold for a while. We see room for further Fed easing in late 2026 if energy prices cool.

- Asia

Asia retains a mild easing bias through 2026 with the bulk of rate cuts already behind us. In fact, high oil prices may be skewing the calculus towards tightening. Meanwhile, robust economic momentum is putting upward pressures on KTB and MGS yields.

- US Dollar Index

Three drivers are contributing to a mildly negative USD outlook: US-ROW growth gap is narrowing, US equities continue to underperform global peers, and elevated policy uncertainty.

- G7

German fiscal stimulus may show up in Eurozone growth, providing support for the EUR. The RBA is leading global central banks into a new rate hike cycle, while others are still contemplating rate cuts. Relative central bank arguments favour AUD as the conviction long call.

- Asia

The PBOC now appears keener on moderate RMB strength, allowing the USD-CNY to drift lower. This sets a positive overarching tone for other Asian currencies. SGD should find renewed upside as resilient growth compels the MAS to price out easing policy actions in favour of potential tightening moves this year.

- Private Equity

Private equity is increasingly about capturing value earlier in the corporate lifecycle, with buy-and-build operating improvement replacing leverage-led models. Entry points look more attractive as valuations sit at a decade-low compared to public markets, with small- to mid-market deals offering the clearest balance of value and execution.

- Private Credit

Private credit offers a higher yield against public high yield. IG senior-secured structures provide downside protection, although investors should pay attention to distinguish IG private credit from exposures in Broadly Syndicated Loans (BSLs) and Business Development Companies (BDCs) which can embed equity-like risk.

- Hedge Funds

Hedge funds continue to offer diversification and alpha potential as geopolitical fragmentation and policy shifts drive changing volatility regimes. Macro strategies can exploit cross-market dislocations, while relative-value and long/short equity benefit from dispersion, as evident in the recent software rout.

- Gold

We stay bullish gold as debasement risk and geopolitical uncertainty tailwinds intensify, driving increased hedging behaviour by investors.

- Commodities

The commodities rally is broadening after gold’s outsized gains. Favour commodities that benefit from scarcity, national security priorities, and long-term structural demand.

2Q26 CIO Asset Allocation (CIO AA)

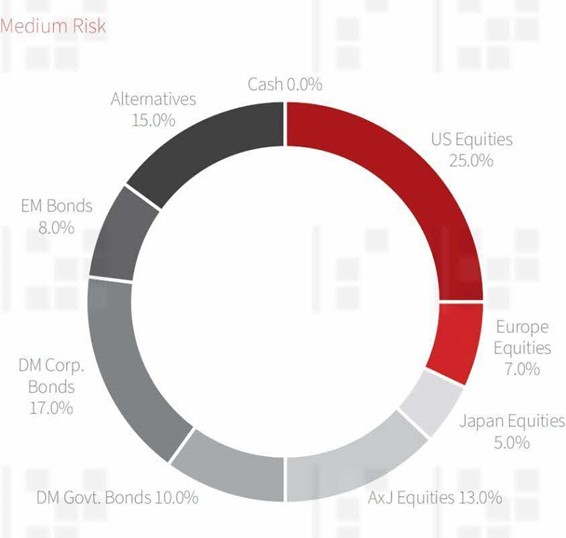

CIO AA Breakdown by Asset Class (Medium-Risk Profile

About DBS

DBS is a leading financial services group in Asia with a presence in 19 markets. Headquartered and listed in Singapore, DBS is in the three key Asian axes of growth: Greater China, Southeast Asia and South Asia. The bank's "AA-" and "Aa1" credit ratings are among the highest in the world.

Recognised for its global leadership, DBS has been named “World’s Best Bank” by Global Finance, “World’s Best Bank” by Euromoney and “Global Bank of the Year” by The Banker. The bank is at the forefront of leveraging digital technology to shape the future of banking, having been named “World’s Best Digital Bank” by Euromoney and the world’s “Most Innovative in Digital Banking” by The Banker. In addition, DBS has been accorded the “Safest Bank in Asia” award by Global Finance for 17 consecutive years from 2009 to 2025.

DBS provides a full range of services in consumer, SME and corporate banking. As a bank born and bred in Asia, DBS understands the intricacies of doing business in the region’s most dynamic markets.

Established in 1989 as part of the Singapore-based DBS Group, PT Bank DBS Indonesia (Bank DBS Indonesia) is one of the banks with the longest history in Asia. Currently operating 1 Operational Head Office, 13 Branch Offices, 14 Sub-Branch Offices, 32 ATMs spread across major cities and 2.861 active employees in 15 major cities in Indonesia, Bank DBS Indonesia provides comprehensive banking services that focus on the customer experience to 'Live more, Bank less'. We also see a purpose beyond banking and are committed to supporting our customers, employees, and the community towards a sustainable future.

PT Bank DBS Indonesia is licensed and supervised by The Indonesian Financial Services Authority (OJK), and an insured member of Indonesia Deposit Insurance Corporation (LPS).

DBS is committed to building lasting relationships with customers, as it banks the Asian way. Through the DBS Foundation, the bank creates impact beyond banking by uplifting lives and livelihoods of those in need. It provides essential needs to the underprivileged, and fosters inclusion by equipping the underserved with financial and digital literacy skills. It also nurtures innovative social enterprises that create positive impact.

With its extensive network of operations in Asia and emphasis on engaging and empowering its staff, DBS presents exciting career opportunities. For more information, please visit www.dbs.com.

DBS Group

Useful Links

Awards

World's Best Bank 2025, 2018 - 2022

Euromoney, Global Finance, The Banker

Asia’s Safest Bank, 2009 – 2025

Global Finance