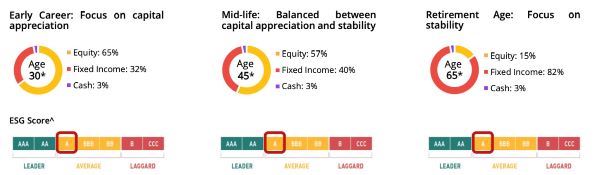

How it worksFor a customer aged 30, the portfolio would focus on leveraging the benefit of a longer investment horizon to achieve greater capital appreciation by allocating greater exposure to equities (65%) versus fixed income (32%) and cash (3%). With the passing of time, the portfolio will gradually de-risk from this skew, to hold more in fixed income instead. When the customer finally nears his or her pre-determined retirement age of 65 (as an example, since age is customisable), the portfolio would have reduced equity exposure (15%) and a heavier weight towards fixed income (82%), which provides more stability and cushions the investment against market volatility.

Prior to DBS Retirement digiPortfolio, investors looking to invest in such a manner would incur frequent transaction or switching costs, as they transition from one portfolio mix to the next in preparation for retirement. DBS Retirement digiPortfolio investors pay only a flat 0.75% annual management fee, which allows them to benefit from a fully automated experience with the glidepath strategy and enjoy other features, such as making recurring top ups and withdrawals at any time. A portfolio can be created with a minimum one-time SGD 1,000 lump sum investment, and customers can subsequently choose to top-up their portfolio monthly with as little as SGD 100. They are also not subject to a sales charge, lock-in period, or withdrawal penalties.The portfolio, which is professionally managed by the DBS Chief Investment Office and JPMAM, is an extension of the bank’s years-long effort to lower barriers of entry to investing and democratise retail investors’ access to wealth management services.“DBS Retirement digiPortfolio is designed with careful risk calibration over decades in mind. This effectively breaks down big hurdles for customers who want to plan for retirement, yet find it too daunting. It also serves to remove some of the inertia we hear around retirement planning, by making it not only more accessible to all but also more affordable to start with,” said Ling Seng Chuan, Head of Financial Planning, Insurance and Investment, DBS Bank. “When markets become volatile as retirement nears, it can put a damper on years of otherwise diligent retirement planning. We can help mitigate this through our holistic retirement planning proposition, where DBS Retirement digiPortfolio complements other passive income such as CPF Life and insurance annuities, so that our customers can ultimately feel more secure with well-diversified and optimised retirement plans.”Jacklyn Goh, Head of Singapore Intermediaries, J.P. Morgan Asset Management, said: “Achieving financial independence and retiring meaningfully will be on the mind of investors as countries like Singapore, confront an ageing demographicshift. Acknowledging the personalised needs for each individual’s retirement is critical in helping investors find the right balance of having a stable and growing portfolio to help achieve their retirement goals. We are excited to partner with DBS to introduce an industry-first personalised retirement proposition for Singapore investors planning for their retirement needs. The personalised feature is what sets this retirement solution apart and brings retirees’ experience to the next level – we are proud to enable the customisation leveraging our investment insights, technology resources and model-advisory portfolio capabilities.”Ng Bing Hua, a pilot investor aged 34, said: “Most of my existing investments require monitoring and research, and this takes up a good portion of my free time. I chose DBS Retirement digiPortfolio because I enjoy the ease of access via digibank, and unlike other investment products, it had no lock-in or withdrawal penalty should I need to access these funds for an emergency. The portfolio is comprehensive as it had provided me with an idea of how much I need to set aside to attain my ideal retirement payout to complement government schemes like CPF Life. I also trust the expertise of the DBS and JPM investment teams in terms of portfolio composition, and to rebalance and de-risk the portfolio based on market outlook as I age. This is a service that I believe is typically only available to UHNW clients, and so it’s great that I get to enjoy it as well.”“We are very heartened by our customers’ positive response to the pilot, and especially by the fact that 70% of them have committed to making recurring top-ups to their portfolios. It affirms our belief that we are on the right track in getting our customers interested in planning for the longer term. We look forward to helping more of our younger salaried customers take advantage of their longer retirement runway by not only starting to invest now, but also adopting a consistent, disciplined approach to investing that prioritises time in the market, rather than timing the market,” added Ling.Customers can sign up for the DBS Retirement digiPortfolio conveniently via DBS/POSB digibank. For more information on DBS Retirement digiPortfolio, please visit here or here.