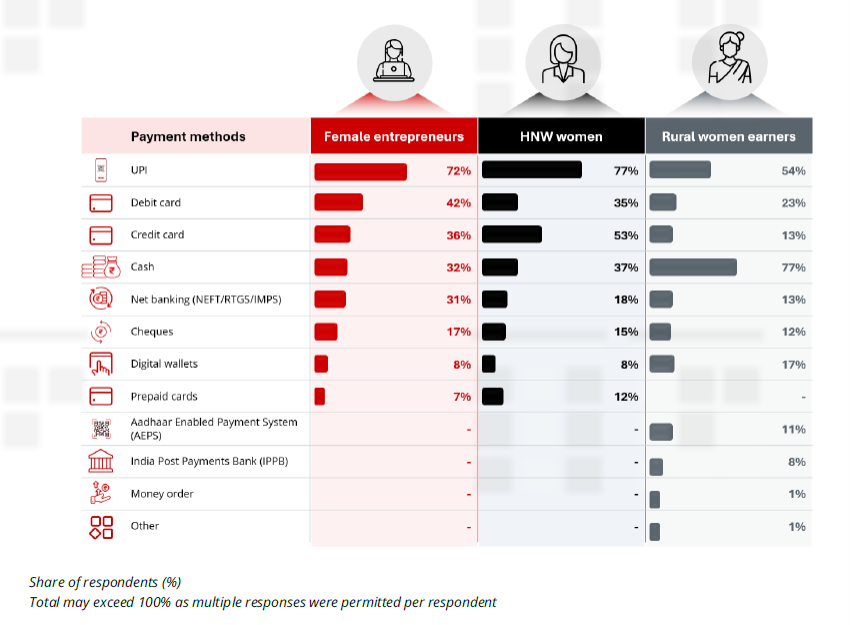

Most used digital payment methods

UPI is the leading digital payment method among female entrepreneurs (72%) and HNW women (77%). While rural women earners continue to rely on cash for everyday transactions, more than half (54%) also use UPI.

Beyond UPI, payment preferences diverge by cohort. Credit cards are the second most used payment method among HNW women (53%), while female entrepreneurs rely more on debit cards (42%).

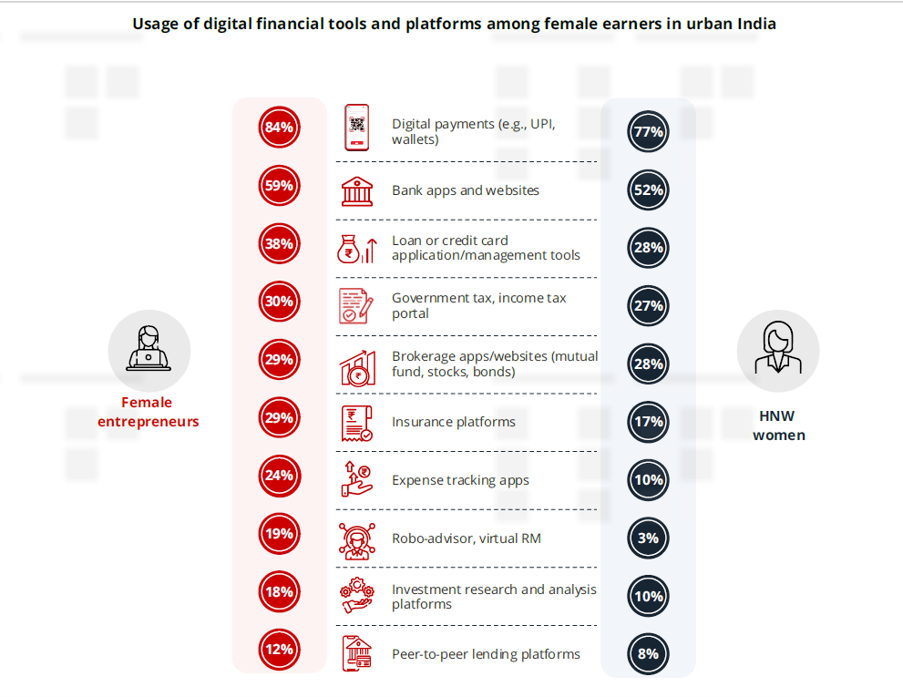

Beyond payments: Adoption of digital platforms and tools

Beyond banking and payments, female entrepreneurs are increasingly engaging with a wider ecosystem of digital financial tools and platforms. Among those surveyed, 38% use loan and credit platforms, while 29% use brokerage platforms. Among HNW women surveyed, 28% are actively using brokerage platforms for their investments, reflecting growing comfort and proficiency in using digital investment tools, driven by the convenience and accessibility they offer.

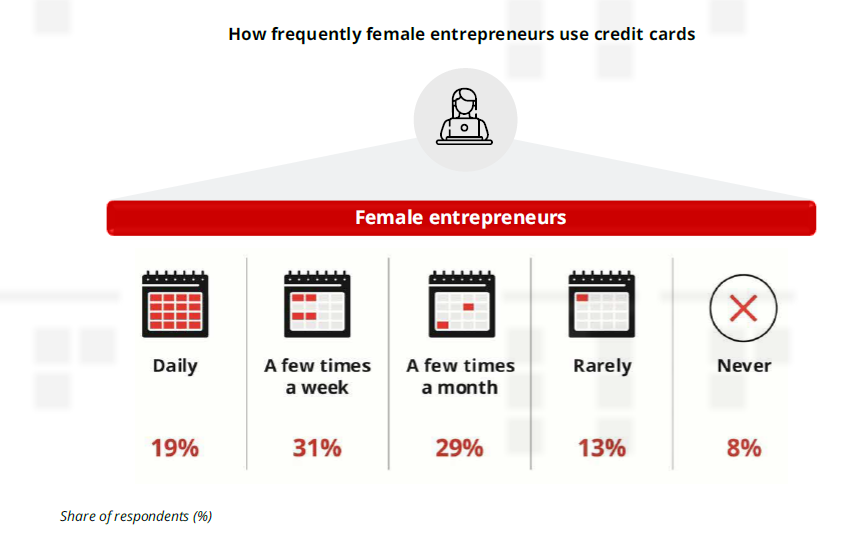

Frequency of credit card usage: Female entrepreneurs

Among the female entrepreneurs surveyed, half of the respondents used their cards frequently, either daily (19%) or a few times a week (31%).

The frequency of credit card usage among female entrepreneurs varies across cities. Bengaluru and Hyderabad report the highest share of daily users (25% each), compared with the national average of 19%. Frequent credit card usage (a few times a week) is particularly prominent in Delhi, where 43% of female entrepreneurs report this behaviour, compared with the national average of 31%.

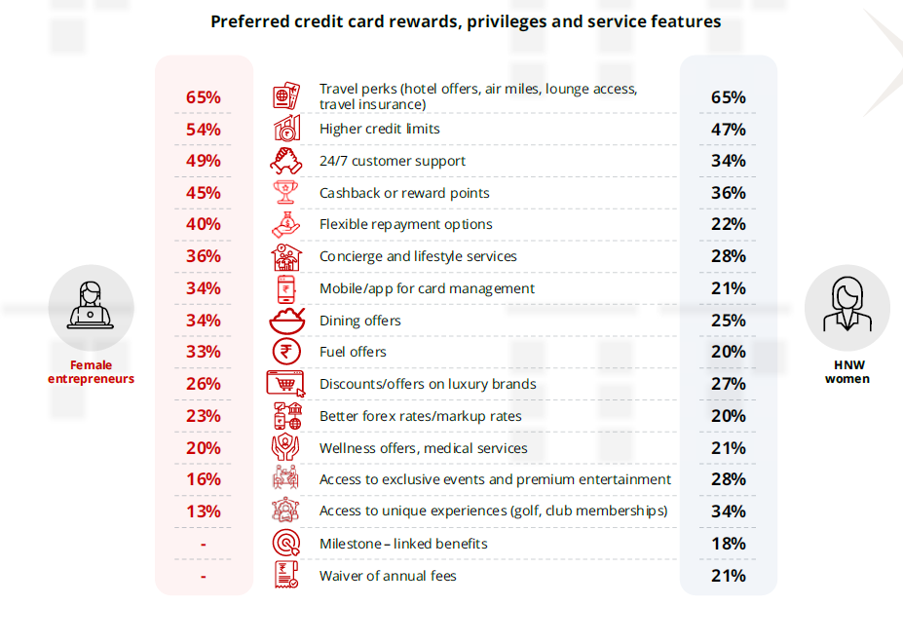

Customer expectations from credit cards: Female entrepreneurs and HNW women

Travel perks emerge as the most preferred credit card benefit among female earners in urban India. Nearly two-thirds of both female entrepreneurs (65%) and HNW women (65%) selected travel perks ahead of other benefits, with preference rising to 70% among HNW women aged 25–30 years and 68% among female entrepreneurs aged 26–35 years.