- Banking

- Wealth

- Privileges

- NRI Banking

- Treasures Private Client

Related Insights

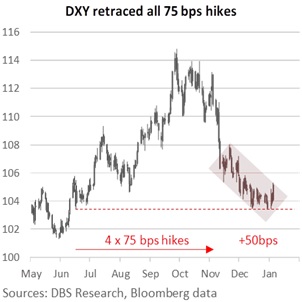

DXY appreciated 0.9% to 105.14, slightly above the 103.4-105 range set after the smaller 50 bps Fed hike to 4.25-4.5% in mid-December. Fed Presidents started 2023 by pushing back the market’s bets for rate cuts later this year. Esther George (Kansas City) sees the Fed Funds Rate (FRR) holding above 5% into 2024. Neel Kashkari (Minneapolis) wants the FFR to rise to 5.4%, above the 5.1% pencilled in last month’s Summary of Economic Projections. James Bullard (St Louis) reckoned more hikes will be necessary for the policy rate to be sufficiently restrictive. Today, Raphael Bostic (Atlanta), Thomas Barkin (Richmond), and George will discuss the outlook while Fed Governor Lisa Cook tackles inflation. Next Tuesday, all eyes will be on Fed Chair Jerome Powell at the international symposium organized by Sweden’s Riksbank.

Although US CPI inflation fell to 7.1% YoY in November from its peak of 9.1% in June, the Fed still considers it too high above its 2% target. The IMF warned that US inflation has yet to turn the corner despite expecting a third of the world to be in recession. The Fed attributed the initial fall in inflation from its peak to the drop in goods inflation and easing supply disruptions. The Fed needs to see progress in the other two inflation components – housing and core services. Inflation from the housing sector needs time to work through the backlog of new rent renewals. More importantly, the tight labour market remains challenging to bring down inflation in non-housing related core services, which accounts for 55% of the PCE core deflator. Hence, pay attention to prices paid in today’s ISM services PMI report.

Understandably, markets are nervous about today’s US monthly jobs report. Although consensus expects nonfarm payrolls to slow to 203k in December from 263k in November, ADP employment did jump to 235k (vs 150k consensus) from 182k (revised from 127k). Initial jobless claims also fell to 204k (vs 225k consensus) for the week ending 31 December from 223k the previous week. With the unemployment rate low at 3.7%, average hourly earnings growth is strong, around 5% YoY. DXY can recoup more lost ground if a still-robust jobs report withdraws bets for a smaller 25 bps hike at the FOMC meeting on 1 February in favour of a second 50 bps hike. If DXY pushes above its price channel, it could hold a higher 105-107 range.

Quote of the day

“I am always ready to learn although I do not always like being taught.”

Winston Churchill

6 January in history

Vietnam held its first general election in 1946.

Topic

Explore more

E & S Macro StrategyThe information herein is published by DBS Bank Ltd and/or DBS Bank (Hong Kong) Limited (each and/or collectively, the “Company”). This report is intended for “Accredited Investors” and “Institutional Investors” (defined under the Financial Advisers Act and Securities and Futures Act of Singapore, and their subsidiary legislation), as well as “Professional Investors” (defined under the Securities and Futures Ordinance of Hong Kong) only. It is based on information obtained from sources believed to be reliable, but the Company does not make any representation or warranty, express or implied, as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions expressed are subject to change without notice. This research is prepared for general circulation. Any recommendation contained herein does not have regard to the specific investment objectives, financial situation and the particular needs of any specific addressee. The information herein is published for the information of addressees only and is not to be taken in substitution for the exercise of judgement by addressees, who should obtain separate legal or financial advice. The Company, or any of its related companies or any individuals connected with the group accepts no liability for any direct, special, indirect, consequential, incidental damages or any other loss or damages of any kind arising from any use of the information herein (including any error, omission or misstatement herein, negligent or otherwise) or further communication thereof, even if the Company or any other person has been advised of the possibility thereof. The information herein is not to be construed as an offer or a solicitation of an offer to buy or sell any securities, futures, options or other financial instruments or to provide any investment advice or services. The Company and its associates, their directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned herein and may also perform or seek to perform broking, investment banking and other banking or financial services for these companies. The information herein is not directed to, or intended for distribution to or use by, any person or entity that is a citizen or resident of or located in any locality, state, country, or other jurisdiction (including but not limited to citizens or residents of the United States of America) where such distribution, publication, availability or use would be contrary to law or regulation. The information is not an offer to sell or the solicitation of an offer to buy any security in any jurisdiction (including but not limited to the United States of America) where such an offer or solicitation would be contrary to law or regulation.

This report is distributed in Singapore by DBS Bank Ltd (Company Regn. No. 196800306E) which is Exempt Financial Advisers as defined in the Financial Advisers Act and regulated by the Monetary Authority of Singapore. DBS Bank Ltd may distribute reports produced by its respective foreign entities, affiliates or other foreign research houses pursuant to an arrangement under Regulation 32C of the Financial Advisers Regulations. Singapore recipients should contact DBS Bank Ltd at 65-6878-8888 for matters arising from, or in connection with the report.

DBS Bank Ltd., 12 Marina Boulevard, Marina Bay Financial Centre Tower 3, Singapore 018982. Tel: 65-6878-8888. Company Registration No. 196800306E.

DBS Bank Ltd., Hong Kong Branch, a company incorporated in Singapore with limited liability. 18th Floor, The Center, 99 Queen’s Road Central, Central, Hong Kong SAR.

DBS Bank (Hong Kong) Limited, a company incorporated in Hong Kong with limited liability. 13th Floor One Island East, 18 Westlands Road, Quarry Bay, Hong Kong SAR

Virtual currencies are highly speculative digital "virtual commodities", and are not currencies. It is not a financial product approved by the Taiwan Financial Supervisory Commission, and the safeguards of the existing investor protection regime does not apply. The prices of virtual currencies may fluctuate greatly, and the investment risk is high. Before engaging in such transactions, the investor should carefully assess the risks, and seek its own independent advice.