- Banking

- Wealth

- Privileges

- NRI Banking

- Treasures Private Client

- In 3Q, we see the lower levels of Asia swaps as attractive levels to re-establish pay positions.

- KRW, THB and INR swaps offer the best risk-reward to pay…

- …The respective central banks could show relatively more resolve in fighting inflation risks.

- KRW Rates: BOK is more hawkish, and its inflation challenge is relatively larger.

- HKD Rates: Hibor-Libor convergence is likely to occur slower than currently priced.

Related Insights

Recent outsized declines in Asia swap rates and yields have sparked speculation that Asia rates have peaked and a correction in hike overpricing is already underway.

In the early stages of Asia hike cycles, Asia swaps (OIS/IRS) tend to overprice on the pace and quantum of expected rate hikes. And at some time later in the cycle, there will come a "turn" when markets realize that the cycle is approaching an end, and the overpricing in swaps will start to correct towards fairer levels. In our view, we don't think that we have reached such a "turn" yet, and see the bias is still for Asia swaps add back hike pricing in 3Q.

One, it is not clear if we have seen peak Fed hawkishness. There has been some recent softness in US-related economic indicators, and on the back of that, we could see the Fed slightly tone down its hawkish stance. But we think it’s too early to judge that the Fed will soon shift its focus from inflation risks to growth concerns.

Two, we have not seen peak Asia inflation yet. So far in July, we have gotten June inflation prints for Indonesia, Thailand, South Korea, the Philippines and China. The read-across is that Asia inflation prints are still rising and surprising to the upside (relative to the survey). Asia central banks' inflation estimates/projections also suggest that YoY prints are expected to continue to rise, and a peak is still in front of us.

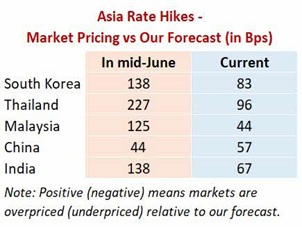

We proxy market pricing of peak policy rates via 1y forward swap-implied rates and compare them against our economist forecast. In mid-June, we saw that Asia swaps were grossly overpriced by more than 100bps of additional hikes. Since then, market fears around growth and recession risks and the possible implications for global hike paths have seen overpricing come down significantly. We think the current swap pricings are much closer to fair. The current low level of overpricing (relative to mid-June) and our belief that rates are biased higher ahead mean that current swap rates present better entry points to selectively initiate payers.

Accordingly, we hold a pay on further dips stance in KRW, THB and INR swaps. Compared to regional peers, we think that the respective central banks of those markets would show relatively more resolve regarding their focus on fighting inflation risks.

We think the risks ahead around Asia inflation and actual hike paths are likely balanced. Asia central banks could get more concerned about the increased passthrough from FX depreciation to domestic inflation, and hence quicken their hike pace. On the other hand, the recent pullback in oil and commodity prices could lessen worries around the persistence of inflation and allow some relief of hike pressures.

For our running Asia rates ideas, we 1) pay 5y CNY NDIRS and 2) receive 5y INR NDOIS ideas initiated in early June. Both ideas are currently in the money. For the pay 5y CNY NDIRS idea, we decide to tighten the take-profit level from 2.95% to 2.85%. The rebound in CNY rates could be smaller than we had expected, as China's growth recovery seems to be more gradual and lockdown risks still linger in the near term. For the receive 5y INR NDOIS idea, we keep the take-profit level at 6.65% and could look to flip to pay if the profit-taking level is hit.

We add the following two new ideas.

- Pay 2y KRW NDIRS (TP 3.70%, SL 2.85%)

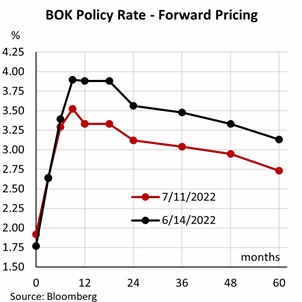

The Bank of Korea (BOK) is one of the more hawkish central banks in the region, communicating its urgency and commitment to tackle inflation. Headline CPI printed 6.0% YoY in June, the highest in more than 20 years. BOK survey also shows that 12m forward inflation expectations amongst South Koreans hit 3.9% in June, the highest reading in almost 10 years. The inflation challenge is also compounded by the won's faster depreciation pace (most in Asia over the last 12 months) which could mean relatively larger pass-throughs to import prices and CPI.

Our economist is forecasting back-to-back BOK hikes at the July and August meeting. The BOK's larger inflation challenge has also led to some market expectations of more aggressive 50bps hikes. Looking at onshore FRAs, markets have priced in a 50bps hike for July and 25bps hike for August meetings. For October and November meetings, FRAs are pricing for 35-70% chances of 25bps hikes per meeting. Compared to mid-June, markets' hike pricing has decreased considerably, by around 50bps. We think the pullback in hike pricing presents better entry levels to reload swap payers, as the risks to inflation and BOK's hike path remains firmly tilted to the upside.

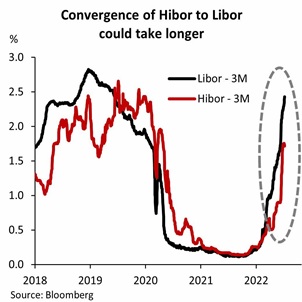

- Receive 2y HKD IRS vs pay 2y USD IRS (TP -0.55%, SL +0.15%)

Our idea is centred on the view that the convergence of 1m/3m Hibor to Libor will occur at a slower pace than what is currently priced by markets. At present, 3m Hibor (1.71%) is around 70bps below 3m Libor (2.42%). FX forwards and IRS markets are pricing for 3m Hibor to catch up to 3m Libor around 9-10 months from now (i.e., April/May 2023). We think that the convergence process taking longer and so express via a receive 2y HKD vs pay 2y USD IRS idea. In addition, the idea enjoys significant positive carry/roll (17bps over 3 months).

We don't doubt that as the Fed continues to hike rates in the coming months, the bias is for the 1m/3m Libor-Hibor spread to stay wide and encourage buy USD vs sell HKD carry trades. That would expectedly lead to the weak side convertibility undertaking (CU) of 7.85 to be triggered from time to time, causing HKMA to buy HKD and thereby draining interbank liquidity. However, we think that there are offset factors that could see the weak side CU being triggered at a lower-than-expected frequency and the Aggregate Balance could stay large (>HKD100bn) for longer-than-expected. Specifically, the improvement in China's growth outlook (relative to the rest of the world) could be a key source of support for Hong Kong equities (Hang Seng Index has been outperforming global indices) and draw in stronger equity inflows. The associated USD supply could help to keep USDHKD away from 7.85, or at least not let the weak side CU be triggered frequently.

To read the full report, click here to Download the PDF.

Topic

The information herein is published by DBS Bank Ltd and/or DBS Bank (Hong Kong) Limited (each and/or collectively, the “Company”). This report is intended for “Accredited Investors” and “Institutional Investors” (defined under the Financial Advisers Act and Securities and Futures Act of Singapore, and their subsidiary legislation), as well as “Professional Investors” (defined under the Securities and Futures Ordinance of Hong Kong) only. It is based on information obtained from sources believed to be reliable, but the Company does not make any representation or warranty, express or implied, as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions expressed are subject to change without notice. This research is prepared for general circulation. Any recommendation contained herein does not have regard to the specific investment objectives, financial situation and the particular needs of any specific addressee. The information herein is published for the information of addressees only and is not to be taken in substitution for the exercise of judgement by addressees, who should obtain separate legal or financial advice. The Company, or any of its related companies or any individuals connected with the group accepts no liability for any direct, special, indirect, consequential, incidental damages or any other loss or damages of any kind arising from any use of the information herein (including any error, omission or misstatement herein, negligent or otherwise) or further communication thereof, even if the Company or any other person has been advised of the possibility thereof. The information herein is not to be construed as an offer or a solicitation of an offer to buy or sell any securities, futures, options or other financial instruments or to provide any investment advice or services. The Company and its associates, their directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned herein and may also perform or seek to perform broking, investment banking and other banking or financial services for these companies. The information herein is not directed to, or intended for distribution to or use by, any person or entity that is a citizen or resident of or located in any locality, state, country, or other jurisdiction (including but not limited to citizens or residents of the United States of America) where such distribution, publication, availability or use would be contrary to law or regulation. The information is not an offer to sell or the solicitation of an offer to buy any security in any jurisdiction (including but not limited to the United States of America) where such an offer or solicitation would be contrary to law or regulation.

This report is distributed in Singapore by DBS Bank Ltd (Company Regn. No. 196800306E) which is Exempt Financial Advisers as defined in the Financial Advisers Act and regulated by the Monetary Authority of Singapore. DBS Bank Ltd may distribute reports produced by its respective foreign entities, affiliates or other foreign research houses pursuant to an arrangement under Regulation 32C of the Financial Advisers Regulations. Singapore recipients should contact DBS Bank Ltd at 65-6878-8888 for matters arising from, or in connection with the report.

DBS Bank Ltd., 12 Marina Boulevard, Marina Bay Financial Centre Tower 3, Singapore 018982. Tel: 65-6878-8888. Company Registration No. 196800306E.

DBS Bank Ltd., Hong Kong Branch, a company incorporated in Singapore with limited liability. 18th Floor, The Center, 99 Queen’s Road Central, Central, Hong Kong SAR.

DBS Bank (Hong Kong) Limited, a company incorporated in Hong Kong with limited liability. 13th Floor One Island East, 18 Westlands Road, Quarry Bay, Hong Kong SAR

Virtual currencies are highly speculative digital "virtual commodities", and are not currencies. It is not a financial product approved by the Taiwan Financial Supervisory Commission, and the safeguards of the existing investor protection regime does not apply. The prices of virtual currencies may fluctuate greatly, and the investment risk is high. Before engaging in such transactions, the investor should carefully assess the risks, and seek its own independent advice.