- Banking

- Wealth

- Privileges

- NRI Banking

- Treasures Private Client

- Equities: Markets rose slightly amid banking sector chaos; Big Tech gained on interest rate outlook

- Credit: Cash to suffer after Fed pause and lower rates environment provides tailwinds for IG credit

- FX: DXY to end 1Q inside 101-106 range; AUD and CAD trended south amid lower commodity prices

- Rates: Rate cuts potentially needed to ease banking sector outflows; short end yields to stay down

- Thematics: We expect 2023 to be an inflexion point for the technology sector

Related Insights

Global equities rose as US regulators commit to ring-fence banking system stress. Markets shrugged off global banking sector woes after comments from Treasury Secretary Janet Yellen that regulators are prepared to take more action if needed, to stabilise US banks. Global equities were up 1.5%, with Developed Markets and Emerging Markets rising 1.4% and 2.2% respectively.

US equities rose for the week, led Big Tech names; Apple and Microsoft climbed 9% and 12% respectively this month. The S&P 500, NASDAQ, and Dow were up 1.4%, 1.7%, and 1.2% respectively. Europe closed marginally higher after positive comments from European Central Bank (ECB) President Christine Lagarde regarding euro area banking sector resilience; the FTSE 100 and Stoxx 600 gained 1.0% and 0.9%. Asian equities traded gingerly as China industrial output undershot the consensus forecast, the HSI and SHCMOP gained 2.0% and 0.5% for the week.

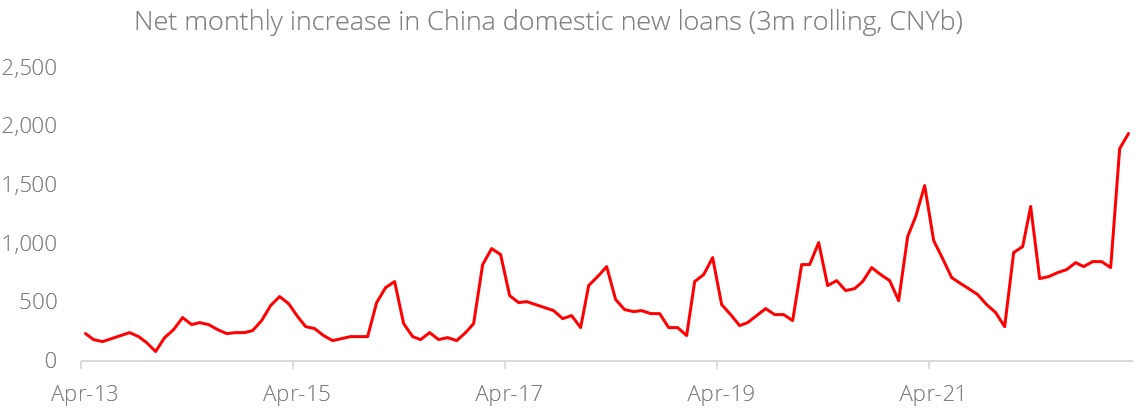

Topic in focus: China financials are an oasis of calm. To support economic revival, Premier Li Qiang announced a 5% GDP growth target for 2023 during the National Party Congress. China financials have been resilient during last year’s market rout as it concluded the year flat despite declines in global (-18%) and Asia ex-Japan equities (-21%).

Unscathed by banking debacle in developed markets. We maintain our constructive stance that China’s large State-owned Enterprise (SOE) banks are insulated from the situations faced by banks in the developed markets, owing to the former’s traditional business models such as domestic centric revenue and balance sheets, anchored by conventional deposits and loans. They are also known for strong local branding and branch networks with access to cheap Current Account Savings Account (CASA) funding, and the discipline to stay away from exotic deposits and loans.

These banks are well positioned as income generators in the CIO Barbell Strategy for their attractive and sustainable dividend yields of 7-8%, supported by the sector’s compelling valuations on the back of stable earnings trend. As such, we continue to advocate China financials as part of a holistic portfolio strategy construct.

Figure 1: China banks’ focused on growing domestic loans

Source: Bloomberg, DBS

Topic

This information herein is published by DBS Bank Ltd. (“DBS Bank”) and is for information only. This publication is intended for DBS Bank and its subsidiaries or affiliates (collectively “DBS”) and clients to whom it has been delivered and may not be reproduced, transmitted or communicated to any other person without the prior written permission of DBS Bank.

This publication is not and does not constitute or form part of any offer, recommendation, invitation or solicitation to you to subscribe to or to enter into any transaction as described, nor is it calculated to invite or permit the making of offers to the public to subscribe to or enter into any transaction for cash or other consideration and should not be viewed as such.

The information herein may be incomplete or condensed and it may not include a number of terms and provisions nor does it identify or define all or any of the risks associated to any actual transaction. Any terms, conditions and opinions contained herein may have been obtained from various sources and neither DBS nor any of their respective directors or employees (collectively the “DBS Group”) make any warranty, expressed or implied, as to its accuracy or completeness and thus assume no responsibility of it. The information herein may be subject to further revision, verification and updating and DBS Group undertakes no responsibility thereof.

All figures and amounts stated are for illustration purposes only and shall not bind DBS Group. This publication does not have regard to the specific investment objectives, financial situation or particular needs of any specific person. Before entering into any transaction to purchase any product mentioned in this publication, you should take steps to ensure that you understand the transaction and has made an independent assessment of the appropriateness of the transaction in light of your own objectives and circumstances. In particular, you should read all the relevant documentation pertaining to the product and may wish to seek advice from a financial or other professional adviser or make such independent investigations as you consider necessary or appropriate for such purposes. If you choose not to do so, you should consider carefully whether any product mentioned in this publication is suitable for you. DBS Group does not act as an adviser and assumes no fiduciary responsibility or liability for any consequences, financial or otherwise, arising from any arrangement or entrance into any transaction in reliance on the information contained herein. In order to build your own independent analysis of any transaction and its consequences, you should consult your own independent financial, accounting, tax, legal or other competent professional advisors as you deem appropriate to ensure that any assessment you make is suitable for you in light of your own financial, accounting, tax, and legal constraints and objectives without relying in any way on DBS Group or any position which DBS Group might have expressed in this document or orally to you in the discussion.

Any information relating to past performance, or any future forecast based on past performance or other assumptions, is not necessarily a reliable indicator of future results.

If this publication has been distributed by electronic transmission, such as e-mail, then such transmission cannot be guaranteed to be secure or error-free as information could be intercepted, corrupted, lost, destroyed, arrive late or incomplete, or contain viruses. The sender therefore does not accept liability for any errors or omissions in the contents of the Information, which may arise as a result of electronic transmission. If verification is required, please request for a hard-copy version.

This publication is not directed to, or intended for distribution to or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or other jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation.

If you have received this communication by email, please do not distribute or copy this email. If you believe that you have received this e-mail in error, please inform the sender or contact us immediately. DBS Group reserves the right to monitor and record electronic and telephone communications made by or to its personnel for regulatory or operational purposes. The security, accuracy and timeliness of electronic communications cannot be assured.