- Banking

- Wealth

- Privileges

- NRI Banking

- Treasures Private Client

- Equities: US equities traded higher as markets expect lower interest rate hikes after banking crisis

- Credit: We reiterate preference for quality credit over cash for risk diversification

- FX: DXY and its components struggled on heightened volatility over banking risks; USD/CNH stable

- Rates: Fed to hike by 25 bps and take FFR to 5%; Terminal rate of 5-5.5% reasonable

- Thematics: We remain constructive on aviation due to the nascent recovery in APAC and promising data

Market traded mixed amid volatility in the banking sector. Volatility dominated sentiments last week (ended 17 March) with major indices turning in mixed performances. This was driven mainly by concerns revolving around the prevailing banking crisis. Global equities were down -0.1%, with Developed Markets remaining flat and Emerging Markets dipping -0.4%.

US equities rose on the back of expectations that the Fed will tone down its hawkish rhetoric amid the current banking fiasco. S&P 500 and NASDAQ gained 1.4% and 4.4% respectively, while Dow dipped -0.1%. Europe ended the week in negative territory on the back of the European Central Bank rate hike and concerns on Credit Suisse’s financial stability. The FTSE 100 and Stoxx 600 lost -5.3% and -3.8% respectively.

Topic in focus: Swiss National Bank’s swift actions to address contagion risks resulting from the failure of a Swiss large bank should safeguard against a systemic banking crisis from materialising. An index of European banks has fallen 12% last week. Despite the takeover by another Swiss Bank in a historic government-brokered deal, we believe the recovery of the sector may take some time as it is unlikely to be immune from potential losses from counterparty risks, increased loss provisions, and capital write-offs, which will have a real impact on earnings and valuations. Going forward, tighter monetary conditions and greater risk awareness will also dampen credit growth and fee. We continue to stay negative on the sector.

We reiterate our Underweight stance in Europe equities. Notwithstanding the current de-risking in markets, we believe there is an opportunity to take positions in some high-quality stocks in the Technology, Luxury, and Healthcare sectors following their recent sharp declines as bond yields head lower.

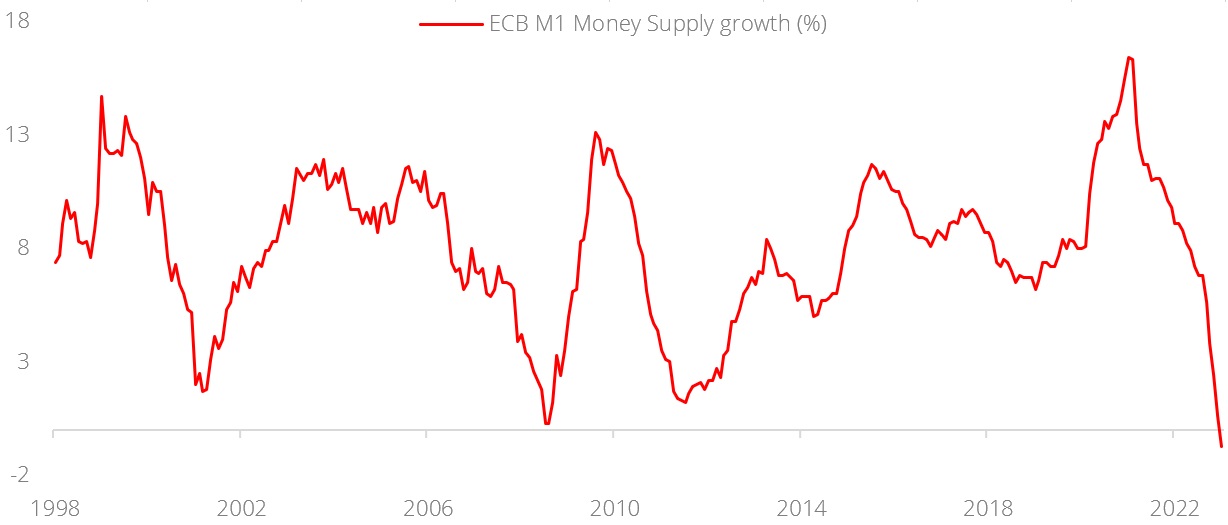

Figure 1: Monetary conditions are already tight, and should tighten further

Source: Bloomberg, DBS

Topic

This information herein is published by DBS Bank Ltd. (“DBS Bank”) and is for information only. This publication is intended for DBS Bank and its subsidiaries or affiliates (collectively “DBS”) and clients to whom it has been delivered and may not be reproduced, transmitted or communicated to any other person without the prior written permission of DBS Bank.

This publication is not and does not constitute or form part of any offer, recommendation, invitation or solicitation to you to subscribe to or to enter into any transaction as described, nor is it calculated to invite or permit the making of offers to the public to subscribe to or enter into any transaction for cash or other consideration and should not be viewed as such.

The information herein may be incomplete or condensed and it may not include a number of terms and provisions nor does it identify or define all or any of the risks associated to any actual transaction. Any terms, conditions and opinions contained herein may have been obtained from various sources and neither DBS nor any of their respective directors or employees (collectively the “DBS Group”) make any warranty, expressed or implied, as to its accuracy or completeness and thus assume no responsibility of it. The information herein may be subject to further revision, verification and updating and DBS Group undertakes no responsibility thereof.

All figures and amounts stated are for illustration purposes only and shall not bind DBS Group. This publication does not have regard to the specific investment objectives, financial situation or particular needs of any specific person. Before entering into any transaction to purchase any product mentioned in this publication, you should take steps to ensure that you understand the transaction and has made an independent assessment of the appropriateness of the transaction in light of your own objectives and circumstances. In particular, you should read all the relevant documentation pertaining to the product and may wish to seek advice from a financial or other professional adviser or make such independent investigations as you consider necessary or appropriate for such purposes. If you choose not to do so, you should consider carefully whether any product mentioned in this publication is suitable for you. DBS Group does not act as an adviser and assumes no fiduciary responsibility or liability for any consequences, financial or otherwise, arising from any arrangement or entrance into any transaction in reliance on the information contained herein. In order to build your own independent analysis of any transaction and its consequences, you should consult your own independent financial, accounting, tax, legal or other competent professional advisors as you deem appropriate to ensure that any assessment you make is suitable for you in light of your own financial, accounting, tax, and legal constraints and objectives without relying in any way on DBS Group or any position which DBS Group might have expressed in this document or orally to you in the discussion.

Any information relating to past performance, or any future forecast based on past performance or other assumptions, is not necessarily a reliable indicator of future results.

If this publication has been distributed by electronic transmission, such as e-mail, then such transmission cannot be guaranteed to be secure or error-free as information could be intercepted, corrupted, lost, destroyed, arrive late or incomplete, or contain viruses. The sender therefore does not accept liability for any errors or omissions in the contents of the Information, which may arise as a result of electronic transmission. If verification is required, please request for a hard-copy version.

This publication is not directed to, or intended for distribution to or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or other jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation.

If you have received this communication by email, please do not distribute or copy this email. If you believe that you have received this e-mail in error, please inform the sender or contact us immediately. DBS Group reserves the right to monitor and record electronic and telephone communications made by or to its personnel for regulatory or operational purposes. The security, accuracy and timeliness of electronic communications cannot be assured.