- Banking

- Wealth

- Privileges

- NRI Banking

- Treasures Private Client

- Equities: Global equities rise against positive macroeconomic backdrop

- Credit: Prefer 3-5 year duration segment to reduce portfolio sensitivity to upward shift in rates

- FX: USD’s sell-off running into technical hurdles as DXY approaches psychological support of 100

- Rates: Market pricing in another 50 bps of hikes followed by subsequent cuts of c.300 bps

- Thematics: Singapore’s real estate sector to grow modestly as economy enters soft patch

Related Insights

Global equities rise as US hits inflation milestone. Global equities rose for a second week in a row as inflation in the US continued to slow; CPI for December fell -0.1% (m/m), representing the largest price decrease since April 2020; headline inflation declined to 6.5% on a y/y basis. Global equities were up 3.3% for the week, with Developed Markets and Emerging Markets gaining 3.2% and 4.2% respectively.

US equities rose last week on the back of easing inflation and positive bank earnings. The S&P 500, Nasdaq, and Dow Jones notched weekly gains of 2.7%, 4.8%, and 2.0% respectively. Europe stocks also edged higher on the back of lower energy prices and China’s re-opening, both of which are expected to buffer the region’s impending economic slowdown; the Stoxx 600 and FTSE 100 rose 1.8% and 1.9% for the week. Asian equities traded higher as China’s December exports fell slightly less than expected (9.9% vs 10.0%); HSCEI and Hang Seng were up 3.5% and 3.6% respectively.

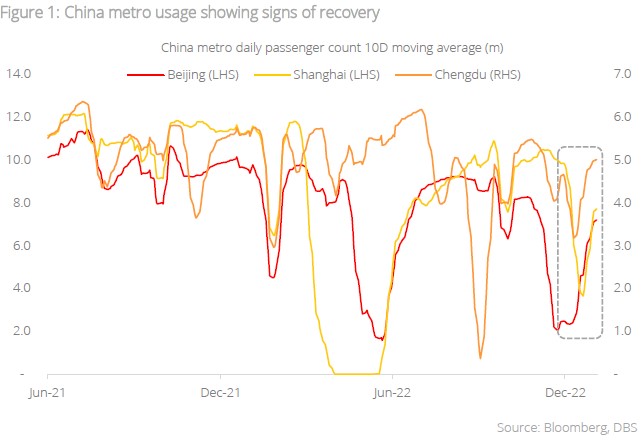

Topic in focus: China reopening picking up pace. Since the announcement on China’s reopening and lifting city-wide lockdowns, there has been consistent improvement in economic activity not only among big cities, but also lower tier cities. This has in turn boosted the investment sentiment and confidence among local consumers. From the end October low, China equities listed in Hong Kong have risen some 50% driven by improvement in outlook and investment managers repositioning to capture the recovery.

One of the barometers of China’s re-opening is mobility data in the form of daily metro passengers among the leading cities of Beijing, Shanghai, and Chengdu (Figure 1). Since the lifting of Covid-19 measures, passenger rides at city metro systems have shown encouraging signs of improvement. We expect the recovery to gain momentum as more business activities regain normalcy. Against this favourable policy backdrop, we maintain our conviction on sectors and themes like technology, domestic consumption, consumer brands, physical retail, and large banks.

Download the PDF to read the full report which includes coverage on Credit, FX, Rates, and Thematics.

Topic

This information herein is published by DBS Bank Ltd. (“DBS Bank”) and is for information only. This publication is intended for DBS Bank and its subsidiaries or affiliates (collectively “DBS”) and clients to whom it has been delivered and may not be reproduced, transmitted or communicated to any other person without the prior written permission of DBS Bank.

This publication is not and does not constitute or form part of any offer, recommendation, invitation or solicitation to you to subscribe to or to enter into any transaction as described, nor is it calculated to invite or permit the making of offers to the public to subscribe to or enter into any transaction for cash or other consideration and should not be viewed as such.

The information herein may be incomplete or condensed and it may not include a number of terms and provisions nor does it identify or define all or any of the risks associated to any actual transaction. Any terms, conditions and opinions contained herein may have been obtained from various sources and neither DBS nor any of their respective directors or employees (collectively the “DBS Group”) make any warranty, expressed or implied, as to its accuracy or completeness and thus assume no responsibility of it. The information herein may be subject to further revision, verification and updating and DBS Group undertakes no responsibility thereof.

All figures and amounts stated are for illustration purposes only and shall not bind DBS Group. This publication does not have regard to the specific investment objectives, financial situation or particular needs of any specific person. Before entering into any transaction to purchase any product mentioned in this publication, you should take steps to ensure that you understand the transaction and has made an independent assessment of the appropriateness of the transaction in light of your own objectives and circumstances. In particular, you should read all the relevant documentation pertaining to the product and may wish to seek advice from a financial or other professional adviser or make such independent investigations as you consider necessary or appropriate for such purposes. If you choose not to do so, you should consider carefully whether any product mentioned in this publication is suitable for you. DBS Group does not act as an adviser and assumes no fiduciary responsibility or liability for any consequences, financial or otherwise, arising from any arrangement or entrance into any transaction in reliance on the information contained herein. In order to build your own independent analysis of any transaction and its consequences, you should consult your own independent financial, accounting, tax, legal or other competent professional advisors as you deem appropriate to ensure that any assessment you make is suitable for you in light of your own financial, accounting, tax, and legal constraints and objectives without relying in any way on DBS Group or any position which DBS Group might have expressed in this document or orally to you in the discussion.

Any information relating to past performance, or any future forecast based on past performance or other assumptions, is not necessarily a reliable indicator of future results.

If this publication has been distributed by electronic transmission, such as e-mail, then such transmission cannot be guaranteed to be secure or error-free as information could be intercepted, corrupted, lost, destroyed, arrive late or incomplete, or contain viruses. The sender therefore does not accept liability for any errors or omissions in the contents of the Information, which may arise as a result of electronic transmission. If verification is required, please request for a hard-copy version.

This publication is not directed to, or intended for distribution to or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or other jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation.

If you have received this communication by email, please do not distribute or copy this email. If you believe that you have received this e-mail in error, please inform the sender or contact us immediately. DBS Group reserves the right to monitor and record electronic and telephone communications made by or to its personnel for regulatory or operational purposes. The security, accuracy and timeliness of electronic communications cannot be assured.