Strong operating performance despite significant

rate headwinds

We achieved another year of strong operating performance despite

the most challenging rate environment in recent years. Total income rose 3% to a record

SGD 22.9 billion as proactive hedging, robust deposit and investment AUM inflows, and our

ability to capture market opportunities across businesses more than offset the

rate pressures. The cost-income ratio was unchanged at 40%, and profit before allowances

increased 2% to a record SGD 13.7 billion. Profit before tax of

SGD 13.1 billion was also a new high. Net profit was 3% lower at SGD 11.0 billion,

reflecting higher taxes from the 15% global minimum tax. Return on equity of 16.2% was

within our 15–17% medium-term target and remained several percentage points above local and

most global peers.

The results underscored the breadth and resilience of our

franchise as we navigated an operating environment shaped by geopolitical rifts and trade

tensions.

The year began on a relatively benign footing, supported by Fed

rate cuts in late 2024 and constructive market sentiment from solid corporate earnings and

steady global growth, but this quickly gave way to a new phase of uncertainty following US

tariff announcements. Resultant movements in interest rates and FX had a material impact on

our performance.

In Singapore and Hong Kong, interest rates declined sharply, even

as the Fed paused rate cuts between December 2024 and September 2025. Sora fell about 160

basis points amid an unusually strong liquidity backdrop, driven by robust foreign inflows

and domestic liquidity accumulation. Hibor also fell by around 160 basis points due

to flush system liquidity conditions. At the

same time, the Singapore dollar appreciated around 2% against the USD, HKD and RMB, and

about 6% against INR and IDR, resulting in FX translation losses on our non-SGD earnings.

Taken together, these interest rate and FX movements created a net interest income headwind

of well over SGD 1 billion for the year.

Net interest income resilience from hedging and

deposit growth

Despite the sizeable headwind, group net interest income was

slightly higher than the previous year at a record SGD 14.5 billion. This reflected two key

factors.

The first was proactive balance sheet hedging. Over the past

three to four years, while interest rates were higher, we acted early to pre-empt the impact

of falling rates by locking in asset yields for longer tenors. Our fixed-rate assets –

comprising fixed-rate mortgages, interest rate swaps and fixed income securities – were

increased by about SGD 70 billion to SGD 210 billion, or one-third of the commercial book.

This positioning reduced our net interest income sensitivity to rate movements

significantly. As at end-2025, net interest income sensitivity stood at

SGD 10 million per basis-point change in

interest rates for the SGD book and negative SGD 4 million per basis-point change for

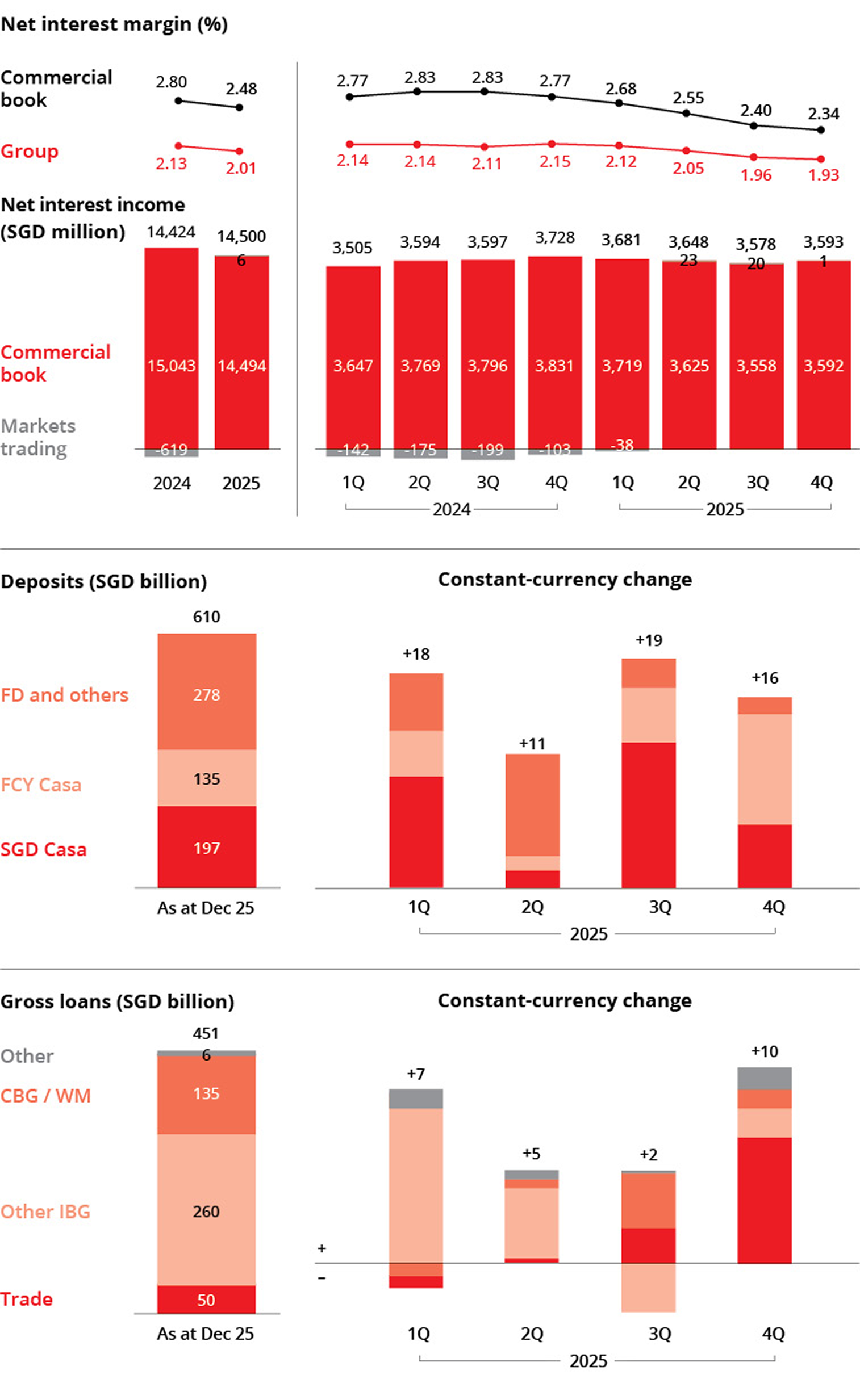

the USD book. For the full year, group net interest margin declined 12 basis points to

2.01%, a smaller compression than local peers, reflecting the benefit of these hedges.

The second factor was robust deposit inflows. Singapore continued

to attract substantial liquidity as a regional wealth hub and financial safe haven, and this

was bolstered by the strong performance of the Singapore dollar against the USD and other

major currencies. With interest rates falling, there was also a shift of retail funds from

treasury bills back into deposits. Deposits grew

SGD 64 billion or 12% in constant-currency terms to SGD 610 billion, the largest absolute

increase in the bank’s history, with over

two-thirds in Casa. The increase in deposits funded loan growth and higher deployment into

liquid assets, both supporting net interest income.

Loans grew SGD 24 billion or 6% in constant-currency terms to SGD

445 billion, driven

by broad-based growth in corporate and non-housing consumer loans. Non-trade corporate loan

pipelines remained healthy despite the uncertain environment, although high repayments in

North Asia tempered growth. Trade loan growth was underpinned by expansion in targeted

client segments, while non-housing consumer loans were led by wealth management lending.

Deposit growth outpaced loan growth, and we nimbly deployed the

excess liquidity into low-risk non-loan assets, including an increase of SGD 42 billion in

HQLA to

SGD 208 billion. While this deployment lowered net interest margins, it was accretive to

earnings and return on equity.

Record non-interest income reflects nimble

execution

and structural strengths

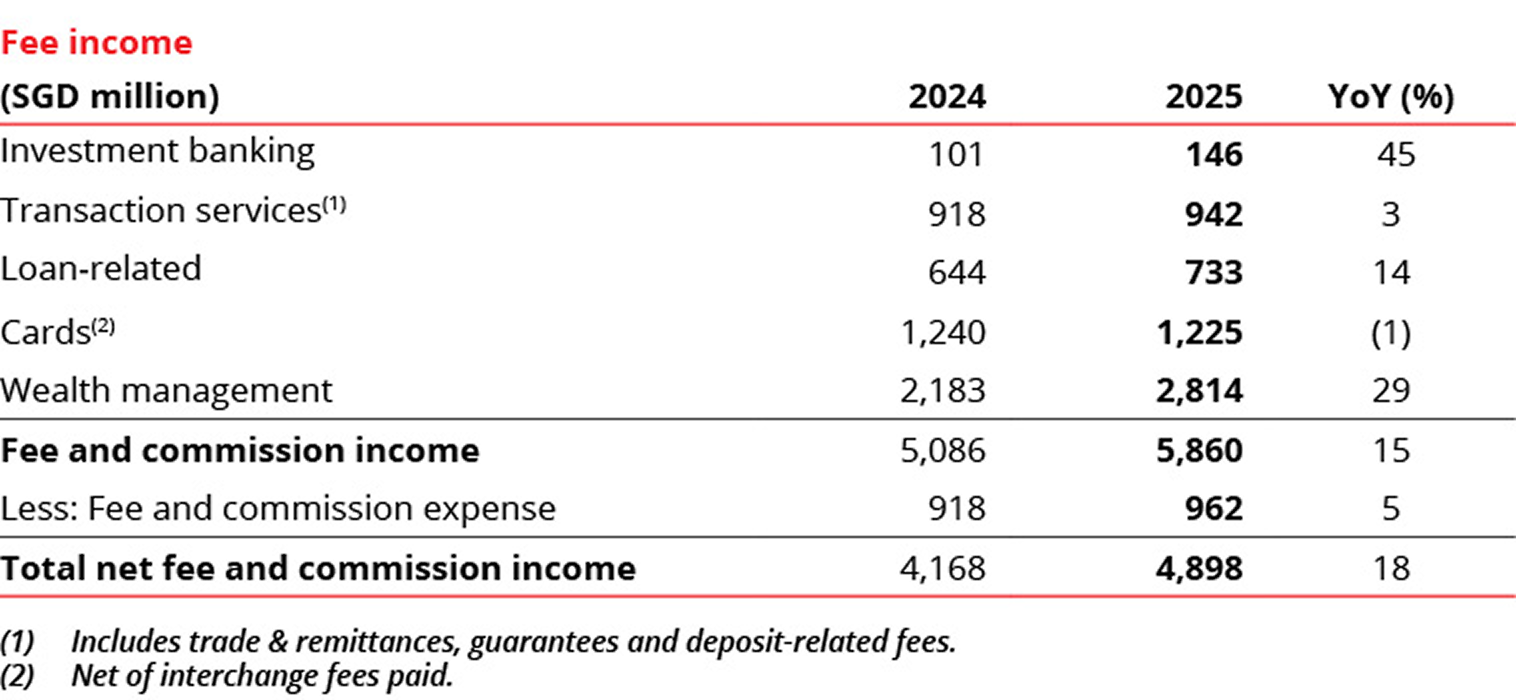

Non-interest income was the main growth engine during the year.

Net fee income rose 18% to a record SGD 4.90 billion, while treasury customer sales

increased 14% to

a new high of SGD 2.14 billion. These gains reflected both cyclical and structural drivers.

Wealth management was the largest contributor to fee growth, with

fees rising 29% to SGD 2.81 billion. After a brief post-Liberation Day soft patch, investor

sentiment recovered as tariff concerns eased and macro and earnings data remained resilient.

Structurally, we benefitted from healthy AUM inflows into Singapore and Hong Kong as global

wealth hubs and from the investments made over the years to deepen our franchise. The Citi

Taiwan integration broadened opportunities in Taiwan, while our refreshed digital wealth

strategy gained traction and supported stronger contributions from retail wealth.

Fee contributions from Institutional Banking also strengthened.

Transaction services fees grew 3% to a record SGD 942 million, supported by higher cash

management fees

from increased payment activity and greater client wallet share, and growth in custody fees

across both traditional securities and digital assets.

Loan-related fees increased 14% to

SGD 733 million, also a new high, reflecting the structural strengthening of our expertise

in target industries and client engagement, even as industry volumes were broadly unchanged.

Investment banking fees rose 45% to

SGD 146 million, as improved capital market conditions supported ECM and DCM deal activity.

Increased capital flows within Asia and between Asia and the GCC created additional

opportunities, and our origination and distribution capabilities positioned us well to

capture these flows.

Treasury customer sales were another key driver of non-interest

income growth, reaching a record level as wealth

management and institutional client demand for investment and hedging solutions rose amid

heightened volatility.

Markets trading non-interest income was 11% lower from a year

ago, though overall markets trading income – combining net interest income and non-interest

income – rose 49% to SGD 1.37 billion, the highest

since 2021. Results were buoyed by periods of higher market volatility following

tariff-related developments, and by stronger treasury customer flows that supported higher

warehousing gains.

Cost discipline and sustained digital leadership

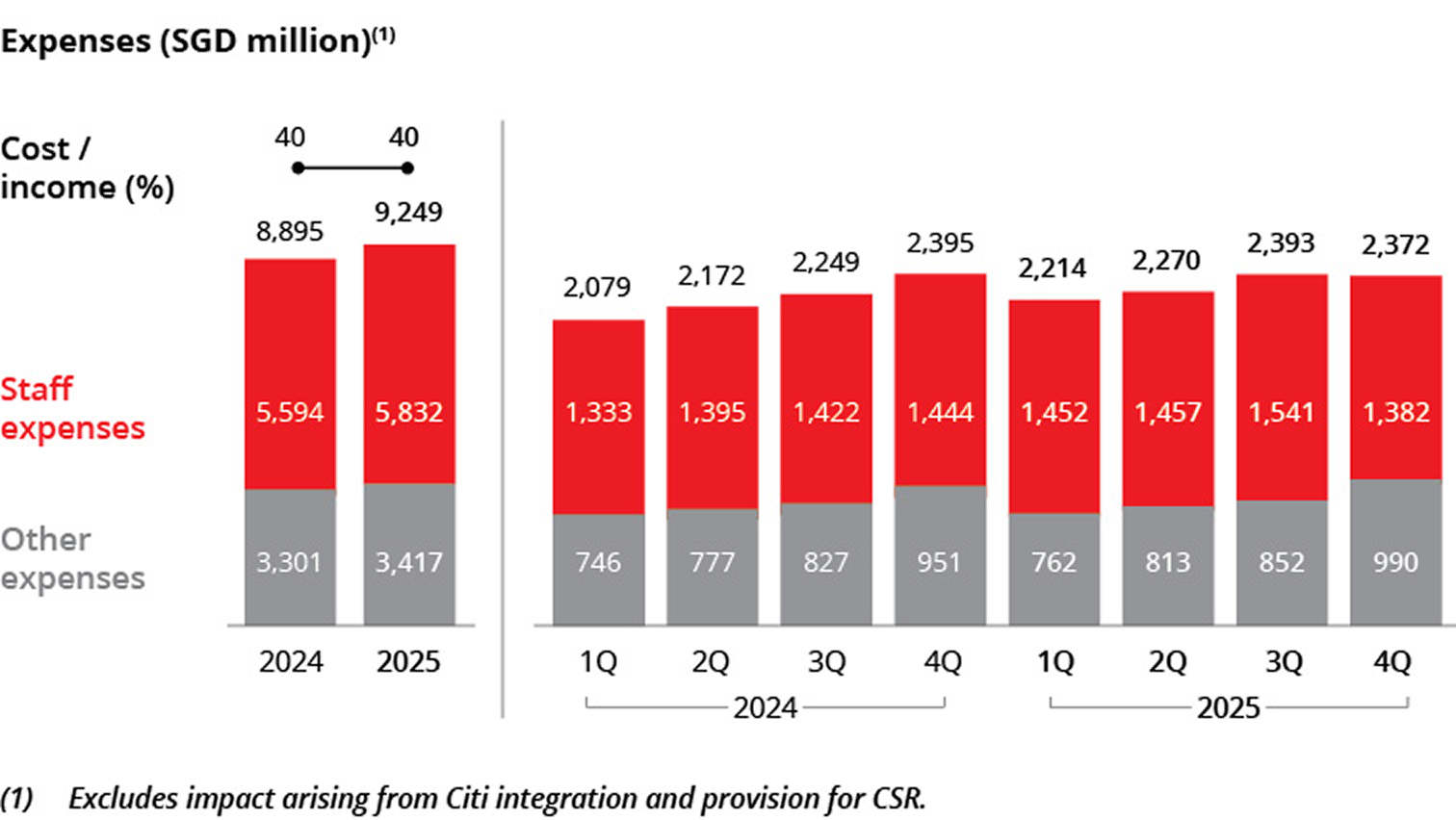

Expenses rose 4% to SGD 9.25 billion led by higher staff costs.

Headcount declined due to reductions in certain overseas markets following the completion of

integration work, while automation and Gen AI adoption supported productivity and contained

resourcing needs. Non-staff expenses were higher mainly from revenue-related items such as

marketing and sales incentives. The cost-income ratio was unchanged at 40%.

DBS has been a first mover in digital transformation, investing

early in digitalisation, data and AI well before the current Gen AI wave, while transforming

the way we work and fostering a strong

innovation culture. These efforts, showcased at our 2017 and 2023 digital investor days,

have delivered tangible improvements in ROE. We will continue to reinvest efficiency gains

into new builds and enhancements to sustain this momentum. Economic impact from data

analytics and AI/ ML was approximately SGD 1 billion in 2025.

Balance sheet remains healthy

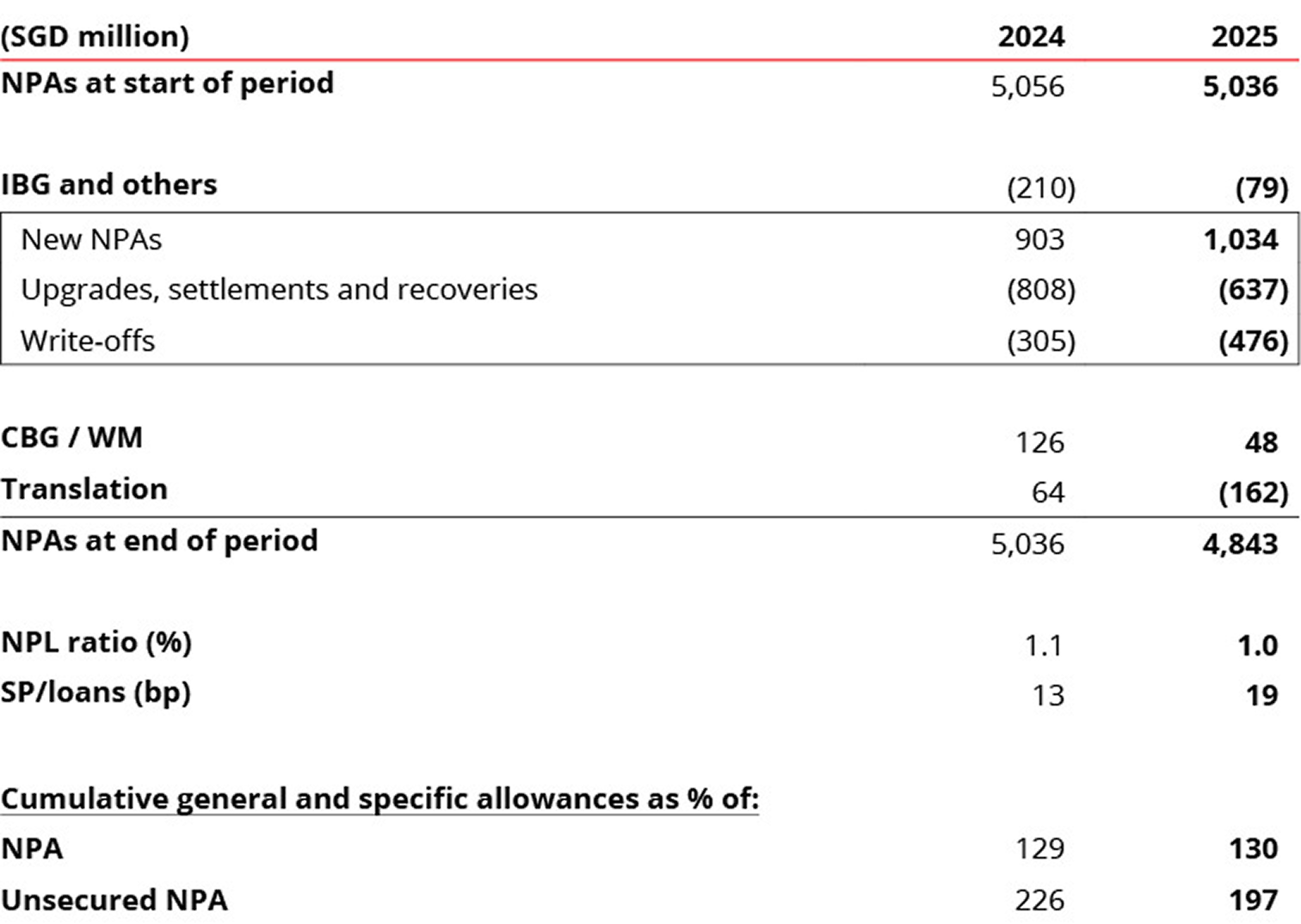

Asset quality was resilient. Non performing assets fell 4%, as

new NPA formation – which included a previously watchlisted real estate exposure prudently

downgraded

to NPL in the fourth quarter – was more than offset by upgrades, repayments and write-offs.

The NPL ratio was stable at 1.0%. Specific allowances amounted to SGD 854 million or 19

basis points of loans, around the historical cycle average.

General allowances of SGD 63 million were written back. There was

an increase in management overlays of around SGD 200 million in the first quarter as a

prudent measure following Liberation Day. This was offset by write-backs over the remainder

of the year, including amounts previously set aside for the real estate exposure downgraded

in the fourth quarter.

Total allowance reserves stood at SGD

6.28 billion, comprising general allowance reserves of SGD 3.86 billion and specific

allowance reserves of SGD 2.42 billion. Allowance coverage was 130%, and 197% after

considering collateral.

Capital remained healthy. The reported Common Equity Tier-1 ratio

was 17.0% based on transitional arrangements. The pro-forma ratio on a fully phased-in basis

was 15.0%. The leverage ratio was at 6.2%, more than twice the regulatory minimum of 3%.

Delivering on our multi-year capital return

commitments

In 2025, we began executing the SGD 8 billion excess capital

return framework announced last year, while continuing to deliver the ordinary dividend

increases guided at our 2023 Investor Day.

The excess capital framework comprises an SGD 3 billion share

buyback programme and SGD 5 billion to be returned through Capital Return dividends of SGD

0.15 per quarter over three years. During the year,

we commenced these initiatives, completing about 12% of the buyback programme, stepping up

repurchases when the share price dipped following Liberation Day.

We also started paying the Capital Return dividend from the first quarter. These initiatives

are intended to reduce our stock of excess capital and are in addition to

our customary progression of ordinary dividends.

For financial year 2025, the Board proposed a final ordinary

dividend of SGD 0.66 per share, an increase of SGD 0.06 from the prior year’s final payout,

and a Capital Return dividend of SGD 0.15 per share, bringing

the total dividend for the year to SGD 3.06 per share, up 38% from the previous year. Taking

the proposed final ordinary dividend of SGD 0.66 per share together with the Capital Return

dividend of SGD 0.15 per share, the annualised total dividend amounts to SGD 3.24 per share.

These distributions are underpinned by our healthy capital position and strong earnings

generation.

Total shareholder returns

Total shareholder returns for the calendar year were 35%,

comprising share price gains of 29% and dividends of SGD 2.85 per share. Dividends paid

included the ordinary dividend for the fourth quarter of 2024 as

well as ordinary and Capital Return dividends for the first three quarters of 2025.

Outlook

2026 is likely to remain a volatile year. Geopolitical fractures,

tariff shocks and fiscal and monetary policy shifts are prompting customers to prioritise

resilience and diversify risks and dependencies, and to partner banks that are stable,

trusted and future-ready to support them through change. DBS is well positioned in this

environment.

We expect total income in 2026 to be around 2025 levels. Fee

income and treasury customer income combined is expected to grow at a high-single-digit rate

as we capture client diversification flows. This should offset a slightly lower group net

interest income, reflecting the full-year impact of lower Sora and a stronger Singapore

dollar, mitigated in part by balance sheet hedges and continued deposit growth.

We expect the cost-income ratio to be in the low-40% range as we

maintain cost discipline.

Specific allowances are assumed to be within 17–20 basis points

of loans. Asset quality remains sound, with general allowance buffers providing resilience

amid ongoing geopolitical and policy uncertainty, and potential for write-backs should

conditions stabilise.

Overall, net profit in 2026 is expected to be slightly below 2025

levels.

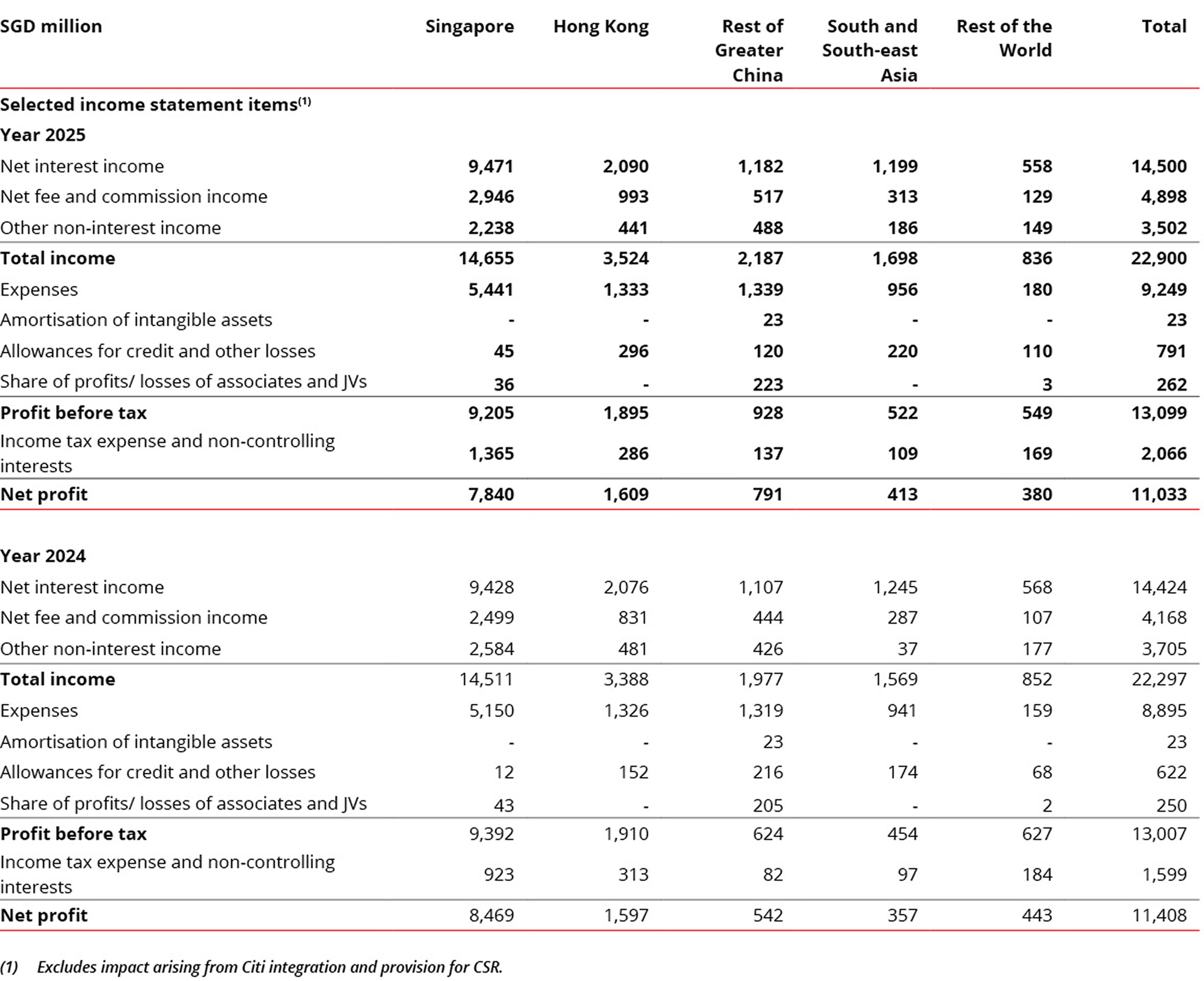

(A) Geographic segment performance

Singapore and Hong Kong, our two largest markets, delivered total

income growth of 1% to SGD 14.7 billion and 4% to SGD 3.52 billion respectively despite

significant rate headwinds. In both markets, net interest income was supported by strong

deposit growth and balance sheet hedging, while non-interest income increased led by wealth

management. Singapore net profit declined 7% to SGD 7.84 billion, due to the impact of the

15% global minimum tax, while Hong Kong net profit rose 1% to SGD 1.61 billion.

Our key growth markets of India, Indonesia, Taiwan and China all

posted double-digit net profit growth, underpinned by robust non-interest income momentum.

South and Southeast Asia total income increased 8% to SGD 1.70

billion. In India, Institutional Banking sustained strong momentum, with growth across

loans, current account balances and treasury customer sales, particularly from large

corporates in GIFT City, while markets trading benefitted from improved market conditions.

Consumer Banking repivoted following regulatory changes, exiting certain ecosystem

partnerships in cards and unsecured lending, while refocusing on segments such as gold

loans, where traction improved in the second half. Indonesia performed well despite a softer

operating environment, as higher non-interest income from FX, derivatives, investment

products and loan fees more than offset net interest margin compression. For the region,

expenses grew 2% to SGD 956 million, while total allowances increased 26% to SGD 220

million. Net profit rose 16% to a record SGD 413 million.

Rest of Greater China total income rose 11% to SGD 2.19 billion.

In Taiwan, the scaled-up franchise following the Citi Taiwan integration and improved sales

productivity supported stronger bancassurance and investment product flows, as well as

higher card fees. Markets trading performance was also robust. In Mainland China, total

income growth was led by non-interest income across wealth management, transaction services,

capital markets and markets trading activities. We continued to deepen our presence in the

Greater Bay Area, including increasing our stake in Shenzhen Rural Commercial Bank to 19.9%.

For the region, expenses grew 2% to SGD 1.34 billion, while total allowances declined 44% to

SGD 120 million. Net profit rose 46% to SGD 791 million.

Geographic segment performance

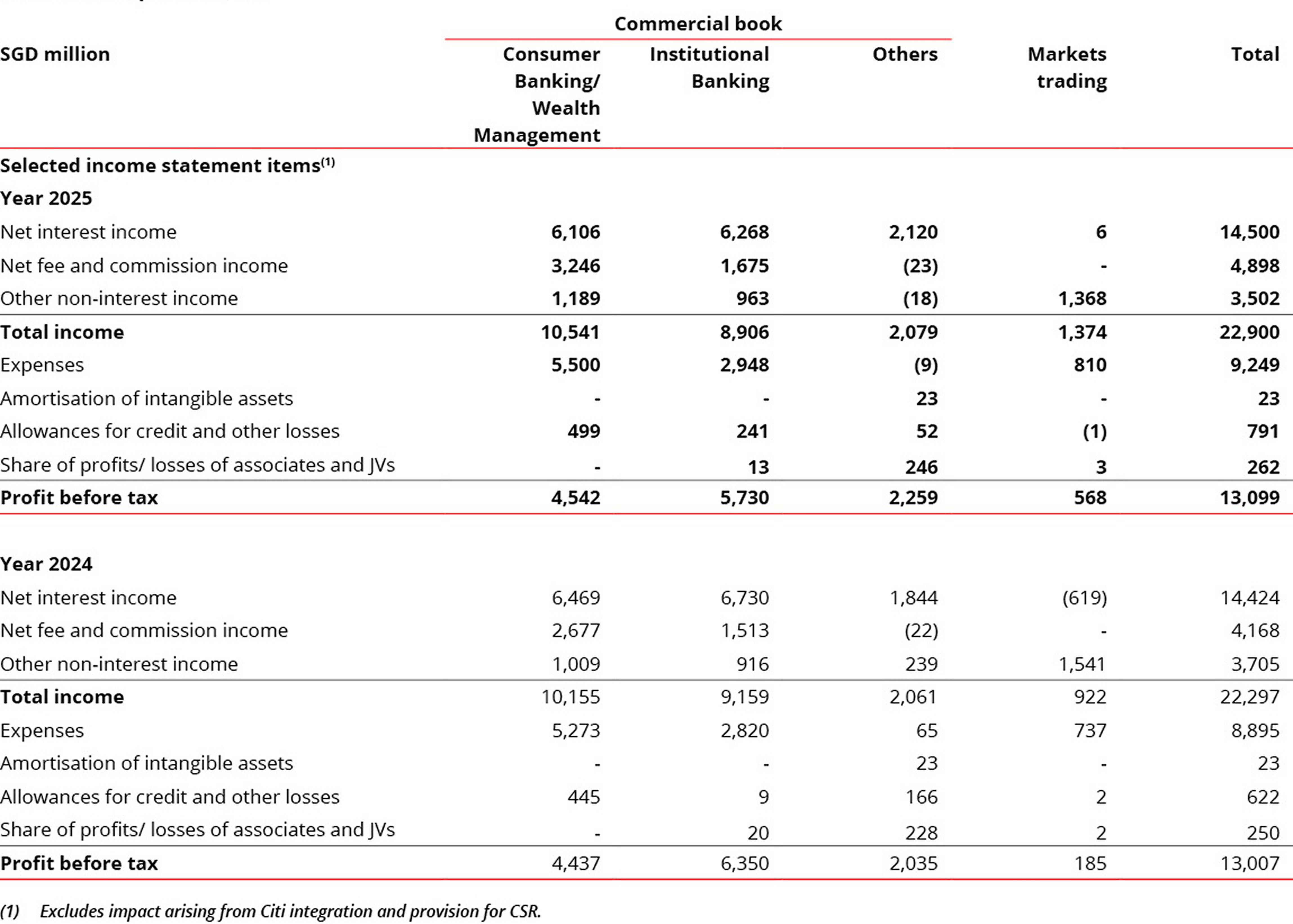

(B) Business unit performance

Consumer Banking/ Wealth Management total income grew 4% to SGD

10.5 billion. Net interest income declined 6% to SGD 6.11 billion as lower net interest

margin was mitigated by volume growth. Non-interest income grew 20% to SGD 4.44 billion led

by double-digit percentage growth in investment and bancassurance fees. Record net new money

inflows of SGD 39 billion drove AUM up 19% in constant-currency terms to

SGD 488 billion. Expenses increased 4% to SGD 5.50 billion, while total allowances rose 12%

to SGD 499 million. Profit before tax grew 2% to SGD 4.54 billion.

Institutional Banking total income declined 3% to SGD 8.91

billion as record loan-related fees, cash management fees and treasury customer income were

offset by lower net interest income. Expenses increased 5% to SGD 2.95 billion. Total

allowances rose by SGD 232 million to

SGD 241 million due to higher specific allowances largely from the real estate NPL in the

fourth quarter. Profit before tax fell 10% to SGD 5.73 billion.

Markets trading income rose 49% to SGD 1.37 billion, the highest

since 2021, with interest rates, equity derivatives and FX activities benefiting from lower

funding costs and a more conducive trading environment. Expenses increased 10% to SGD 810

million. Profit before tax tripled to SGD 568 million.

The Others segment encompasses the results of corporate decisions

that are not attributed to business segments. It includes earnings on capital deployed into

high-quality assets, earnings from non-core asset sales and certain other head office items

such as centrally raised allowances.

Business unit performance

(C) Net interest income

Group net interest income was modestly higher at SGD 14.5

billion, as balance sheet hedging and record deposit growth offset sharp declines in Sora

and Hibor and adverse FX translation from a stronger Singapore dollar. Commercial book net

interest income declined 4% from a lower net interest margin.

Deposits grew SGD 64 billion or 12% in constant-currency terms to

SGD 610 billion, the largest absolute increase in the bank’s history, with over two-thirds

of the increase in Casa. SGD Casa rose as funds from maturing T-bills flowed back into

deposits, while foreign currency Casa growth was broad-based across wealth and corporate

clients.

Gross loans grew SGD 24 billion or 6% in constant-currency terms

to SGD 451 billion, led by broad-based growth in corporate and wealth management loans. As

deposits continued to grow faster than loans, surplus deposits were deployed into liquid

assets, which was accretive to net interest income and ROE.

(D) Non-interest income

Net fee income rose 18% to SGD 4.90 billion. Wealth management

fees increased 29% to a record SGD 2.81 billion. Transaction service and loan-related fees

also reached new highs, while investment banking fees were higher. Card fees were slightly

lower.

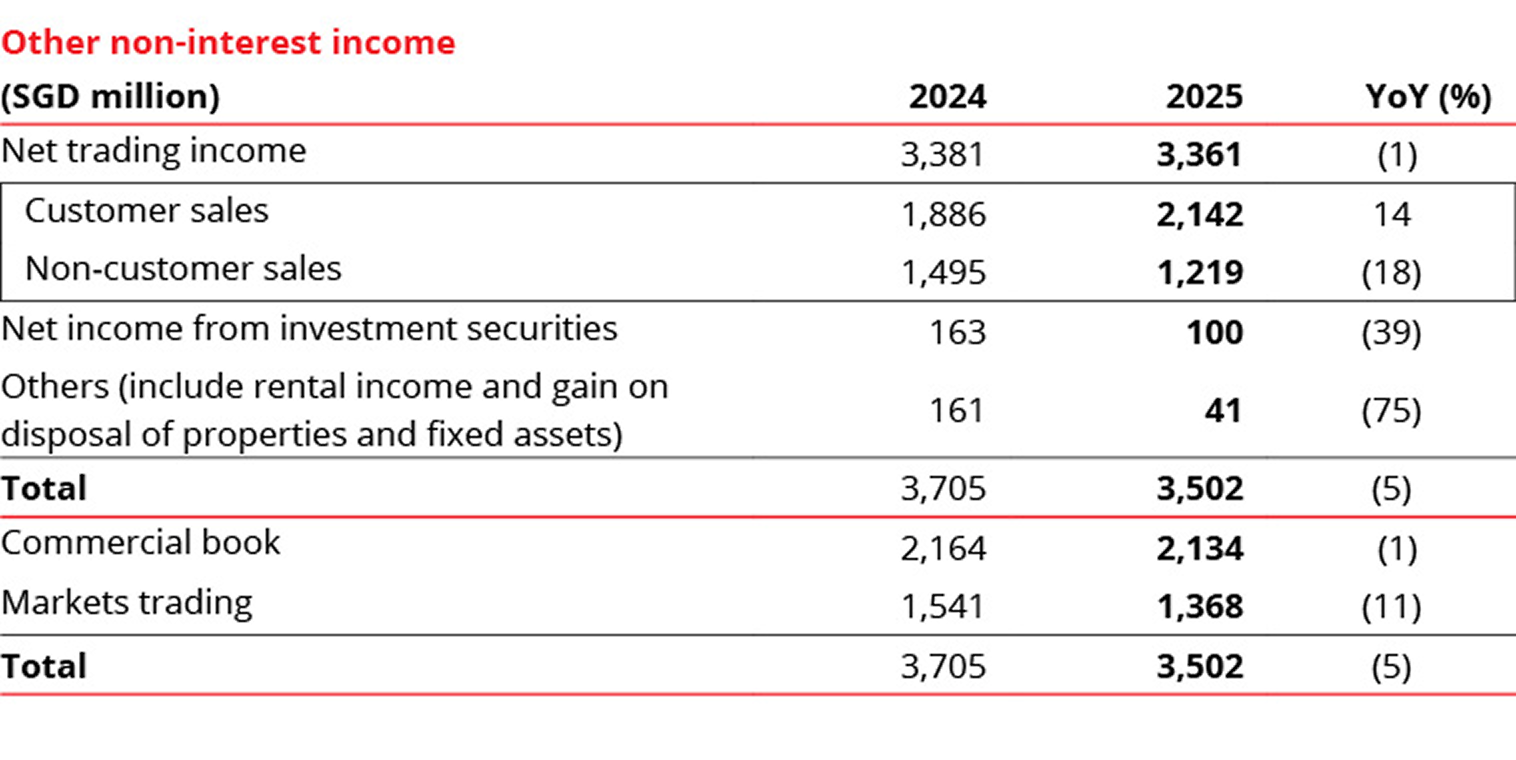

Other non-interest income declined 5% to SGD 3.50 billion as

record treasury customer sales were offset by a decline in non-interest trading income,

lower investment gains and the absence of prior-year non-recurring gains.

(E) Expenses

Expenses rose 4% from a year ago to SGD

9.25 billion led by higher staff costs. The

cost-income ratio was unchanged at 40%.

(F)

Asset quality

Non performing assets declined 4% to SGD 4.84 billion, as new NPA

formation – which included a previously watchlisted real estate exposure prudently

downgraded to NPL in the fourth quarter – was more than offset by upgrades, repayments and

write-offs. The NPL ratio was stable at 1.0%.

Specific allowances amounted to

SGD 854 million or 19 basis points of loans,

broadly in line with the through-cycle

average. General allowances of

SGD 63 million were written back.

Total allowance reserves amounted to

SGD 6.28 billion. Specific allowance

reserves were at SGD 2.42 billion. General

allowance reserves stood at SGD 3.86

billion, which included SGD 2.4 billion of

general allowance overlays. Allowance

coverage was at 130% and at 197% after

considering collateral.

Chng Sok Hui

Chief Financial Officer

DBS Group Holdings